Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Fundamental Differences Between Blockchain and Cryptocurrency

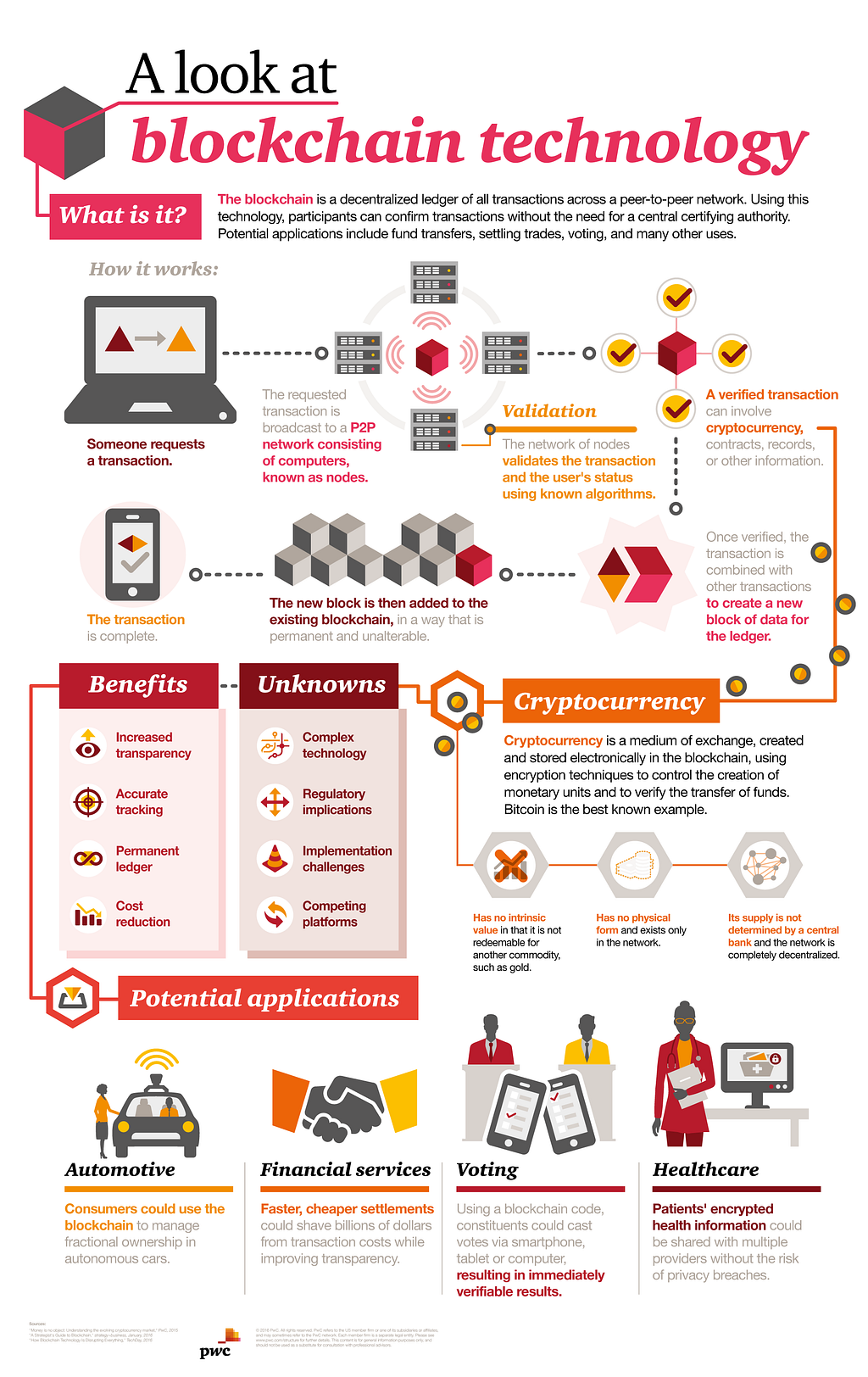

The simplest way to look at Blockchain is that it is the underlying technology that enables Cryptocurrency. It is also used as an alternative for processing massively distributed network transactions. It is a way of sharing very specific values of data, typically stored as a hash value. The data shared is in a non-repudiated format, which means that it is trusted. This trust is not established by a central party, but by multiple parties. For Cryptocurrency, then, trust in the currency isn’t established on the word of a single entity like the Treasury Department; instead, trust is established on the basis of the shared transparent record carried on Blockchain.

Other Uses of Blockchain

Blockchain is a highly hyped technology right now, with forecasts of up to 60% annual growth by 2022, and a worth of $20 billion by 2024. And most of the exploration isn’t into the technology itself, but into its business use. Some of the most interesting business use cases that I’ve seen are in the supply chain area. Specifically, blockchain could be used to identify the fraudulent use of manufacturing components by tagging each component with a private and public key so that its lifecycle can be clearly tracked.

On the consumer side, an interesting possible use of blockchain is to track and maintain our health history. This history belongs to us, not doctors and hospitals, but they do need to be able to access and use it. Blockchain might enable us to maintain our health care histories on the private level, but also make them available as needed.

There’s a similar idea emerging in the Asia-Pacific around using blockchain in higher education to track the diploma GPA of students. It moves the trust location from an institution of higher learning to a broader consensus among the interested parties. Moreover, countries like Japan have already started to look at blockchain to help maintain the authenticity and the entire lifecycle of student’s education experience.

Source: PwC

Source: PwC

Interestingly, blockchain could have been extremely useful to thwart and discourage companies and individuals from becoming victims of instances like the fake diploma scam, that rocked the Middle East and Britain over two years ago.

Fake websites and diplomas from universities that sound and look like they’re legit. Except they’re not!

Fake websites and diplomas from universities that sound and look like they’re legit. Except they’re not!

Factors Slowing Down Adoption of Blockchain

Blockchain holds companies back from Blockchain. The implementation itself is still very limited, even in terms of what you can store. And then you’re not storing everything, just a value of the data. Refining the data just right to get that value out is not easy. It’s just very complex.

Here’s what I think are the three things that are preventing enterprises from Blockchain,

- Business Model

- Right use-cases

- Technical Implementation

Right now there’s no way to do a real-time analysis of Blockchain data, much less analyzing that data along with other business data.

There are two types of use cases,

- New ways of executing existing transactions with blockchain

- New types of transactions that were not possible before

In terms of remedies, one thing that we’re trying to do is bring blockchain into our database processing within DBMS, just like a native data type, so that you can use SQL to process both business and blockchain data. More broadly, we’re looking at the surrounding platform tools and programming languages to help reduce the hurdles of blockchain adoption.

At SAP, we’re really trying to figure out how to simplify the integration of blockchain technology, so that getting value doesn’t necessitate learning this potentially revolutionary technology at a fundamental level.

For enterprises to effectively adopt blockchain, they need an integrated environment where depending on business agreement, execution of transactions on blockchain is an option.

This option is only viable, if these transactions can be then merged with rest of the system of records to provide complete view of activity.

Therefore, SAP is bridging the divide that exists between new type of transaction systems and existing systems of records so customers can adopt innovation without disruption.

If it’s truly revolutionary, why aren’t more top firms doing more with it?

I think that it has a lot to do with the technology viability question. We know that blockchain technology can do these interesting things, but aren’t there any alternative technologies that can provide the same value cheaper and faster? Are we just implementing the technology for the technologies’ sake? Or is it truly driving some use-case scenario or cost-saving that wouldn’t otherwise be possible?

We must stay honest about these questions. The rise of cryptocurrency and the interest around blockchain is exciting, but ultimately it needs to deliver results in business value in its practical applications, that only blockchain can uniquely address. For example, I already foresee the use of distributed databases in private blockchain scenarios — it is cheaper, faster, more data, and can also establish non-repudiated trust. We need to challenge ourselves as an entire blockchain industry consortium to move forward.

How do we actually deliver this? How do we take the promise of Blockchain and make it faster, cheaper, and better? Share your thoughts with me in the comments.

Blockchain and Business Data — A Marriage Waiting To Happen was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.