Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Co-authored by Gary Basin and Taylor Pearson

There’s a lot going on in the world of Bitcoin and it can be hard to keep track of it all. This report aims to offer market participants looking for a one stop shop regarding the current state of Bitcoin.

We cover valuation, technology, regulation/legal, and different ways of getting exposure. This is not meant to read cover-to-cover so if one section is of particular interest, please feel free to skim.

Key Takeaways

Valuation

In general, it should be remembered that we are in the Stone Age for valuation tools for crypto assets and so all valuation models (or collection of models as we’ve presented here) should be taken with a large grain of salt and viewed skeptically.

Having said that, nearly all our indicators suggest that the bear market of 2018 will continue for at least the next few months. Both the NVT and NVM are well into overbought territory and sentiment indicators are predominantly bearish.

Technology

Bitcoin is unique among cryptoassets because there isn’t a whole lot that needs to get done technologically to make it viable as a form of digital gold over the next five to ten years. Even with transaction fees in the tens of dollars, it can still serve as a sovereign-level censorship-resistant store of wealth.

That said, Segwit adoption is up meaningfully which, along with decreased network activity, has brought median transaction fees down under USD $0.10.

Hashrate, an important measure of Bitcoin’s security and censorship resistance is up over 300% YTD.

The Lightning Network is the most talked about technical development on Bitcoin right now but it is probably near the peak of the Gartner hype cycle. There is lots of talk about what can be done with it, but we are probably still at least a couple of years from seeing meaningful adoption.

Long term concerns around fungibility (because of Bitcoin’s limited privacy and pseudonymity rather than anonymity making it possible some coins will be considered “tainted”) and stability of Bitcoin in a future without the mining reward are real but don’t seem like short-term concerns.

Regulation / Legal

Bitcoin is the most regulatory black/white of the cryptoassets. Despite ETF rejections and some companies in the space engaging in regulatory arbitrage, Bitcoin seems to have pretty favorable regulatory tailwinds.

Ways of Getting Exposure

For the investor considering how to get exposure, we divided the vehicles into three buckets

- Non-custodial, Publicly Listed Options available through a traditional brokerage account

- Non-custodial options restricted to accredited investors and high net worth individuals

- Personal custody options

Publicly listed options are still limited and what options there are have significant drawbacks. It seems likely this will change over the next 12 months, though probably not over the next three.

Following the 2017 boom, a handful of non-custodial new options exist for accredited investors and HNWI exist and generally good though investors are forced to choose between low fees and very little customization (cap weighted index funds) or high fees and more customization (actively managed funds).

Personal custody options have not changed much over the last couple of years, perhaps because the options available are generally seen as being pretty good. For individuals institutions choosing to self-custody, a working understanding of operational security is critical.

If you find this report helpful, please let us know. If you would like to receive future versions, please leave us your email to get notified of future editions.

This is a lengthy report. Click here to download a PDF version.

1. Valuation

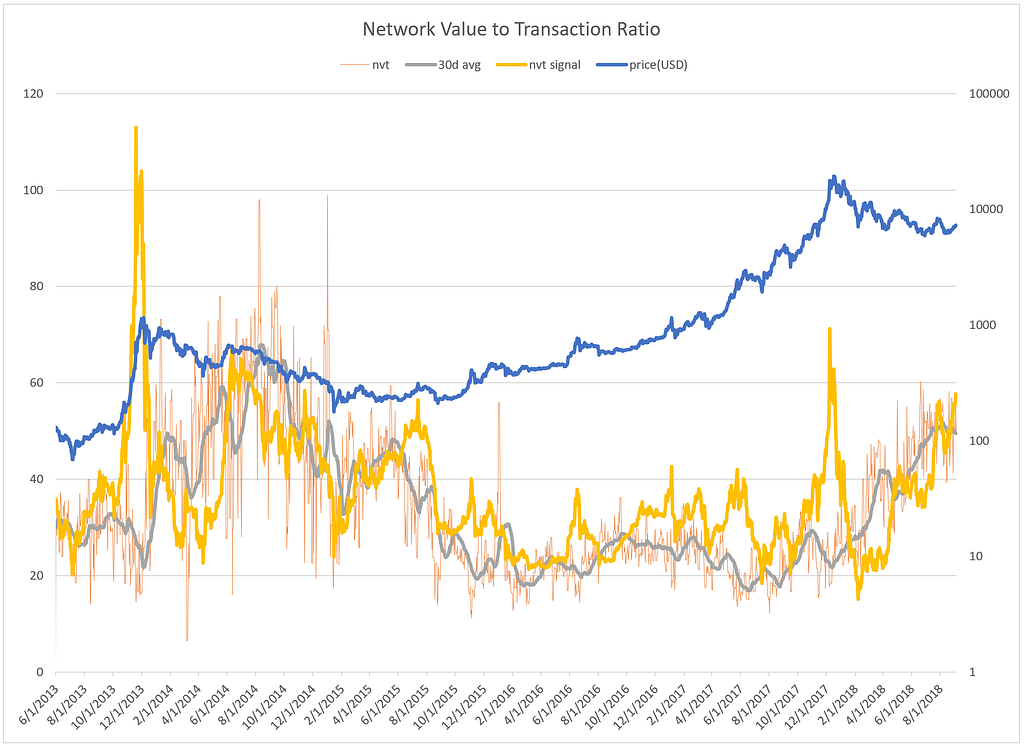

Network Value to Transaction Ratio (NVT)

All data used in calculating NVT and NVM can be downloaded here.

Why it makes sense

The NVT ratio was developed by analyst Willy Woo and is billed as Bitcoin’s PE ratio. The NVT measures the network value (market capitalization) relative to the value of cryptoasset transactions. It’s a simple way to compare how the market prices one unit of on-chain transaction.

When you look at a PE ratio for a traditional company, earnings is used as a proxy for the true utility provided by the company. With the NVT ratio, it’s assumed that the daily on-chain transaction volume (but NOT trading activity which is more speculative) is a good proxy for the true underlying value of the network.

Since NVT is quite noisy, we adjust it a few ways. First, we ignore weekend transaction volumes as there is significant seasonality — weekend volumes are much lower than weekday volumes. Second, we smooth the measure due to significant noise in the daily transaction volume (using a 30 day moving average).

An additional proposed variation is the “NVT Signal”. One issue with smoothing the entire NVT value is this reduces its responsiveness to sharp changes in price (Network Value). Instead, we can leave the numerator “raw” and smooth the denominator (in this case, using a 90 day moving average).

In a recent tweet, NVT creator Willy Woo said his latest thing was that “ NVT measures the ratio between short term trader vs long term investor speculation.” Using this thesis, a low NVT ratio suggests relatively more BTC is held by long-term investors and a high NVT ratio suggests relatively more is held by short term traders.

body[data-twttr-rendered="true"] {background-color: transparent;}.twitter-tweet {margin: auto !important;}

We're now at about the same peak levels of NVT as the 2014 detox. In other words, a deviation between Mcap and on-chain value transfer. My latest thinking is perhaps NVT measures the ratio between short term trader vs long term investor speculation. https://t.co/gMvxIBHvxA

function notifyResize(height) {height = height ? height : document.documentElement.offsetHeight; var resized = false; if (window.donkey && donkey.resize) {donkey.resize(height); resized = true;}if (parent && parent._resizeIframe) {var obj = {iframe: window.frameElement, height: height}; parent._resizeIframe(obj); resized = true;}if (window.location && window.location.hash === "#amp=1" && window.parent && window.parent.postMessage) {window.parent.postMessage({sentinel: "amp", type: "embed-size", height: height}, "*");}if (window.webkit && window.webkit.messageHandlers && window.webkit.messageHandlers.resize) {window.webkit.messageHandlers.resize.postMessage(height); resized = true;}return resized;}twttr.events.bind('rendered', function (event) {notifyResize();}); twttr.events.bind('resize', function (event) {notifyResize();});if (parent && parent._resizeIframe) {var maxWidth = parseInt(window.frameElement.getAttribute("width")); if ( 500 < maxWidth) {window.frameElement.setAttribute("width", "500");}}

Why it doesn’t

One of the potential flaws of this model is that it assumes transacting is a good proxy metric for the value of Bitcoin as earnings is for a traditional company. It’s not clear that’s the case

It’s not even clear that NVT is even a direct measure of monetary value. Since the network value is the market capitalization, this is equal to the USD$ price per Bitcoin times the total number of Bitcoin in existence.

The Daily Transaction Volume is simply the amount of Bitcoin transacted on-chain (although, see below about adjustments) multiplied by the USD$ price per Bitcoin. If we factor out the Bitcoin price aspect, we are left with NVT = Number of Outstanding Bitcoin / Bitcoin Daily On-chain Volume. Looking at it this way, the NVT doesn’t seem to capture pricing information at all. Rather, it’s a measure of [inverse] velocity — how quickly a Bitcoin is changing hands.

This means that NVT fundamentally looks at the value of Bitcoin as a medium of exchanges. If more and more of the market starts to see Bitcoin as digital gold (which seems to be the case), the value comes not from acting as a medium of exchange but from storing value. Does NVT capture that well? Probably not.

Analysis

Right now BTC is unwinding from the 2017 mania phase, not unlike it unwound in 2014 from the 2013 mania. That means Bitcoin NVT ratios look high and have for most of 2018. BTC is well into overbought territory and has been for most of 2018.

If the NVT and NVS continue to be accurate valuation metrics under the current market paradigm, we still have quite a bit of unwinding to do.

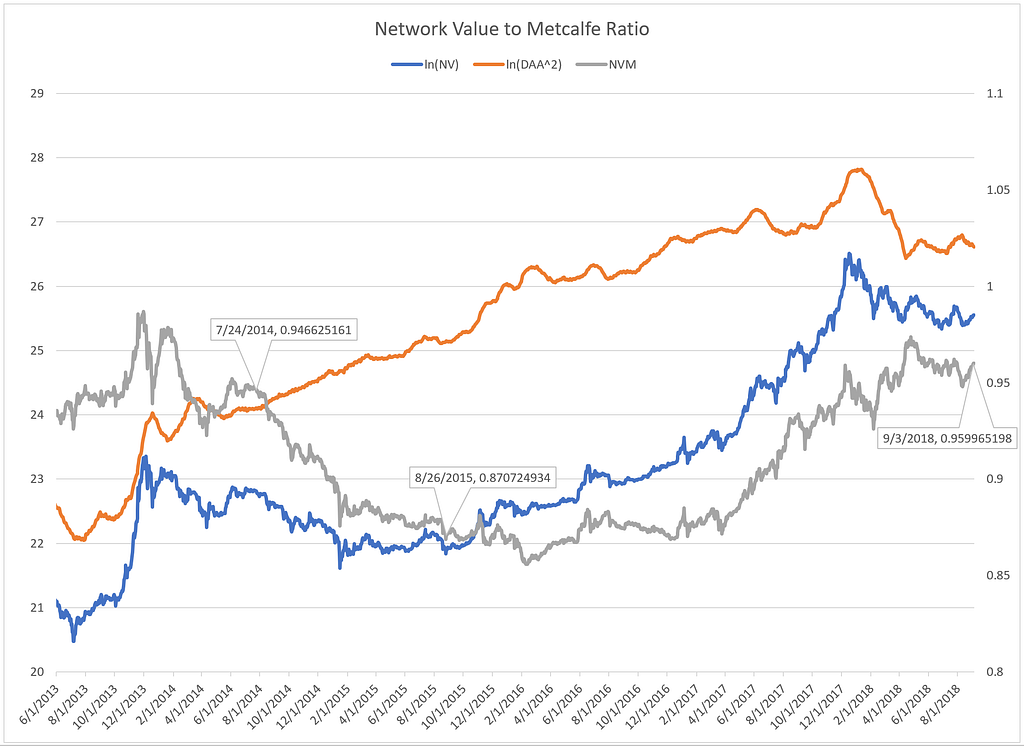

Network Value to Metcalfe Ratio (NVM)

Why it makes sense

Metcalfe’s Law was developed by Robert Metcalfe to explain the relationships between the value of a network and its size. The relationship is based on the idea of a network effect: that for networks, each additional user increases it’s value to others. If there are only two telephones in the world, they are not that useful. As you add more phones, the original two get more valuable.

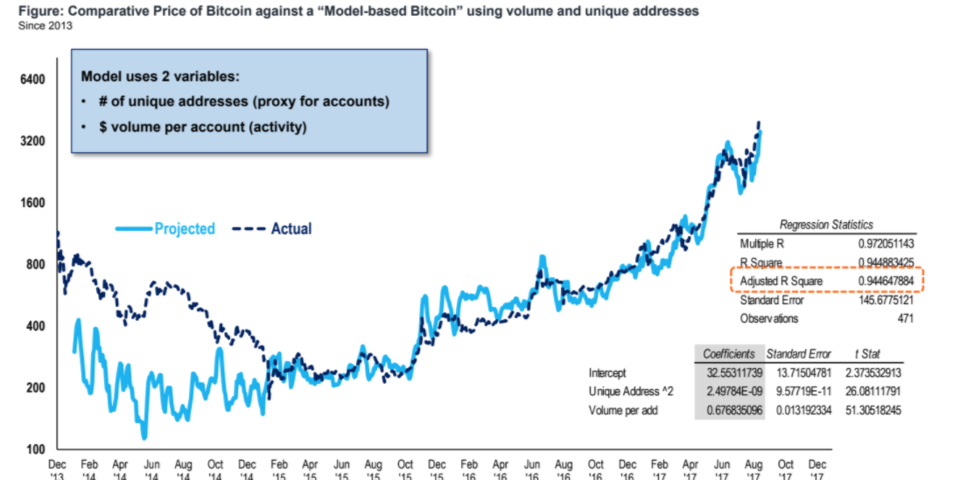

In 2015, Zhang et al. found that Facebook’s revenue was proportional to the square of its monthly active users (MAU). Ken Alabi built off this work to show that Bitcoin, Ethereum and Dash were fairly well modeled by Metcalfe’s law.

It makes sense that Bitcoin exhibits some network effect because it is a form of money and money solves the coincidence of wants problem (essentially that barter is inefficient because people have different needs — e.g. if a musician is paid in beer and his landlord doesn’t accept beer then he can’t make rent, he needs money).

Fundstrat analyst Tom Lee found that as of late 2017, 94% of Bitcoin’s price movements could be explained by the the NVM (though this looks like bad statistics to us).

Analyst Dmitry Kalichkin came up with a more refined model using two different ways of calculating Metcalfe’s Law which correlated closely with Bitcoin’s price.

The main problem with the above approaches is they are fitting variables for a model using all of the data — of course it will look good in-sample, but does it make sense to use it for prediction?Re

Why it doesn’t

While clearly there is some impact of Metcalfe’s law on Bitcoin, it makes us a bit cautious whenever you assume the old tools (which worked well on previous assets like Facebook and Tencent) will work perfectly for something which shows meaningfully different characteristics.

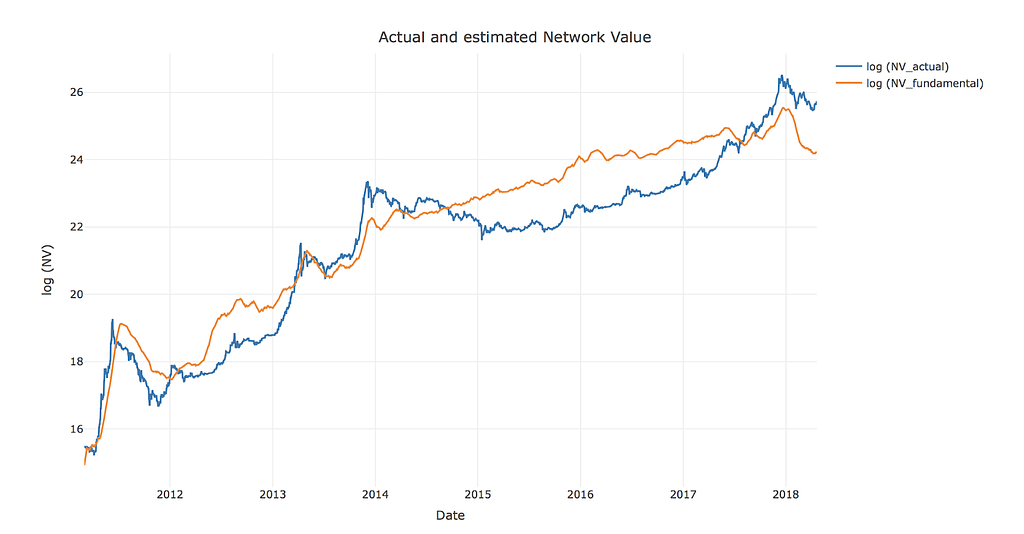

From a price prediction standpoint, it’s also statistically dubious. At first glance, using just Metcalfe’s Law as a predictor (the natural log of Daily Active Addresses squared) ln(DAA²) of the natural log of network value ln(market cap) does not seem to be all that useful. They move approximately together and have similar scales, but this is still a far cry from being a useful market timing tool. To the extent other traders are looking at it, however, it may be relevant for anticipating their behavior.

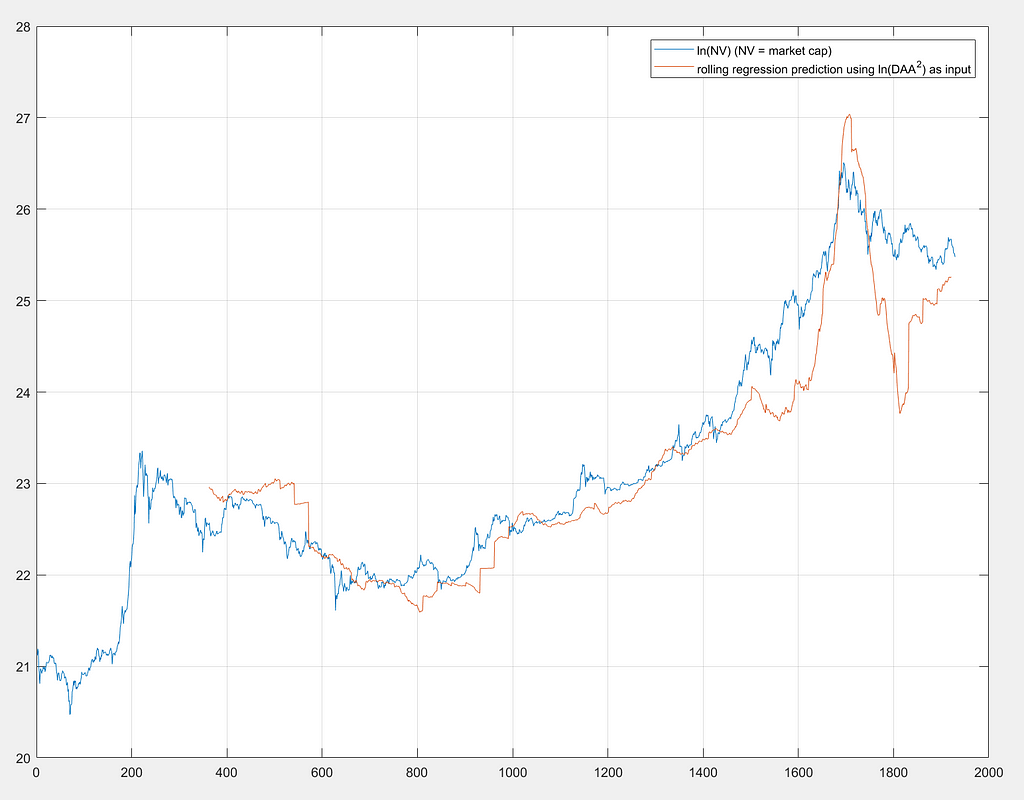

To try to refine it more, we perform a rolling regression to use the ln(DAA²) as a predictor. A rolling regression implies a moving lookback window (360 days here) and prediction window (30 days), such that the betas of the regression are able to update over time to adapt to changing behavior. This also avoids the lookahead and curve fitting biases created by approaches which take into account all the data at once and fit variables that ensure good results — this only works in hindsight.

We can see above that the prediction (out-of-sample, orange line) is not particularly useful as it generally lags behind the target (blue line).

Analysis

Overall, while the current price level is healthier than in December 2017, it still seems quite high relative to Daily Active Addresses. An NVM around 0.95 was previously seen almost a year into the previous bear market — circa August 2014 — and BTC did not enter into a secular bull cycle until about a year later — circa August 2015 — with NVM closer to a value of 0.87.

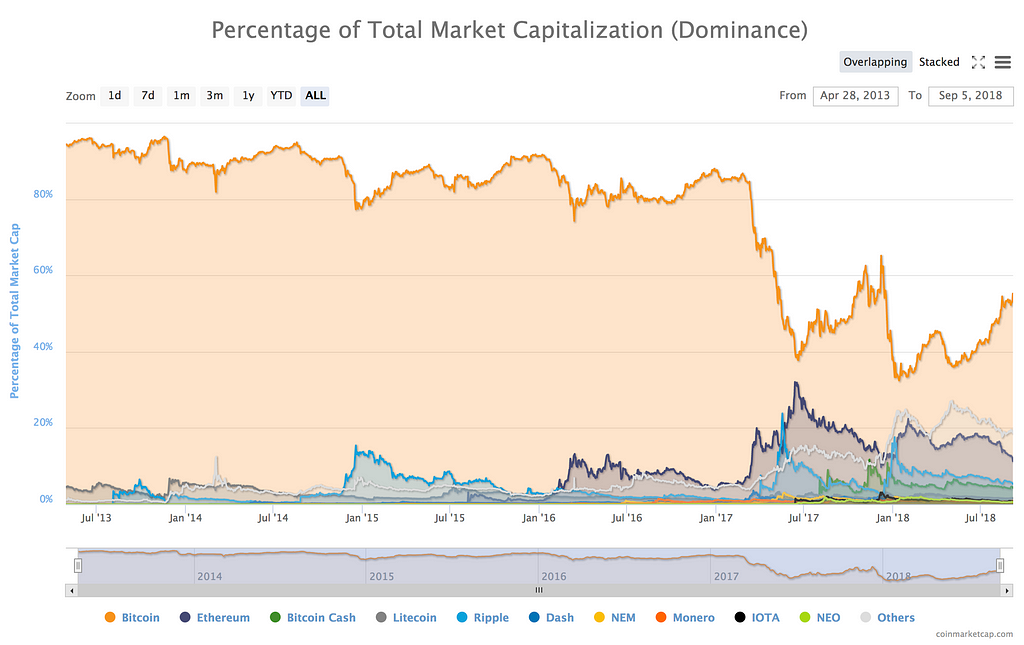

Bitcoin Dominance

Why it makes sense

BTC Dominance measures the percentage of total cryptoasset market capitalization represented by Bitcoin — the reigning king of cryptoassets.

Before the great ICO boom of 2017, Bitcoin dominated the cryptocurrency narrative. There’s some indication that we are shifting back to that world. The Fat Monies thesis — see this explication by Arjun Balaji, argue that the next wave of investors will be focused on money and so Bitcoin is the primary opportunity in the short to medium term. In that world, we may expect Bitcoin to regain dominance from a capital allocation standpoint, with a few other major coins competing for secondary use cases. What we wouldn’t expect is much value accruing to utility tokens (much of the ICO boom) or even less popular protocols (as they fail to generate much utility and also serve as poor candidates for new money).

Why it doesn’t

Even if we can make successful predictions on the Bitcoin Dominance Percentage, we could still lose money if we are only betting on the price of Bitcoin. It’s quite possible that Bitcoin dominance could climb back to the old levels of 80%+ but total cryptoasset market cap may still fall, and Bitcoin prices could continue to fall. To bet directly on this, you would need to create a spread position by shorting (buying) other cryptoassets against a BTC long (short). Tetras capital recently released an Ether short thesis advocating this position.

Analysis

Bitcoin dominance is hovering just over 50% at the moment. For those who don’t buy the Fat Protocol thesis, this could still be a massive buying opportunity. On the other hand, it has already rebounded from lows closer to 30% that we saw earlier this year. Investors that believe other protocols will capture the majority of the value of the cryptoasset space may want to reduce exposure to Bitcoin and diversify into other coins.

Sentiment

Valuing a new asset class is notoriously difficult, and the lack of cash flows generated by most cryptoassets makes this even more tricky. Traditional methods like DCF (Discounted Cash Flows) analysis, simply don’t apply.

One factor that remains relevant though is sentiment. Sentiment is particularly relevant an asset driven primarily by speculation as cryptoassets tend to be and for assets which lack sound valuation models, also the case in cryptoassets.

We examine a few different measures of Bitcoin sentiment below. A drawback to measures of sentiment is that they can change quickly, and so are typically only useful for short-term price predictions.

Bitfinex longs/shorts

Why it makes sense

Margin longs versus margin shorts as reported by Bitfinex.

Source: https://www.tradingview.com/chart/k8IXd6tN/#

Source: https://www.tradingview.com/chart/k8IXd6tN/#

Bitfinex, the exchange, publicly reveals position sizing of margined (leveraged) longs and shorts on their platform. This is an excellent gauge of relative and aggregate positioning of aggressive speculators. In addition to capturing their sentiment, it can also indicate the degree to which we can expect auto-liquidation of over-leveraged positions to be self-reinforcing.

For example, when there is an unusually large leveraged short exposure by speculators, a sharp move up in price might sustain itself by those shorts running out of margin collateral and being forced to liquidate by buying into a rising market (and vice versa for leveraged longs in a falling market).

Why it doesn’t

Bitfinex is only one exchange, so their margined long/shorts data may not be indicative of overall positions of speculators in Bitcoin. In addition, as you can see by glancing at the relationship between the long/short position and BTC price, the relationship is noisy at best. More effort may be required to build a predictive model from this data.

Analysis

Levered short positions are approaching the levels of levered longs — relatively rare in this data set. Historically, this has roughly corresponded with local lows in BTC price.

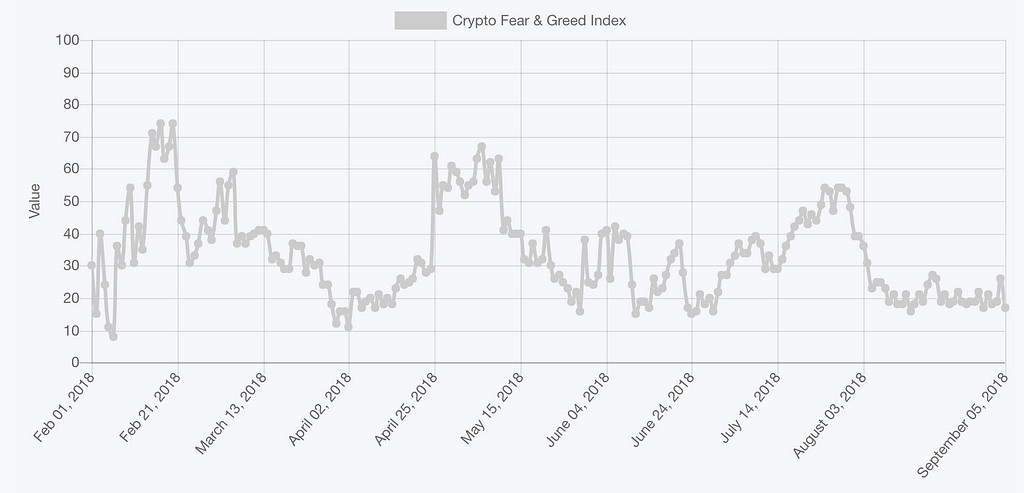

Crypto Fear & Greed Index

Why it makes sense

Alternative.me publishes a proprietary Crypto Fear & Greed Index. It’s composed of market and price factors like volatility and momentum, as well as social media activity, surveys, and other data. With general sentiment indicators, we expect measures of greed to be reaching extremes near market tops, and measures of fear to be reaching extremes near market bottoms.

To the extent these measures are correlated with market participants positions, this can be predictive — when everyone is greedy and already bought in, there are fewer additional buyers available in the market and eventually the greedy start selling (and vice versa for fear).

Source: https://alternative.me/crypto/fear-and-greed-index/

Source: https://alternative.me/crypto/fear-and-greed-index/

BTC over approx same period:

Why it doesn’t

The general problem with these sorts of indicators is that states of extreme greed and fear can persist for extended periods, and revert quickly. For example, we can be at low levels of this index (indicating fear) for several days as price continues to fall, and then it quickly reverts to neutral levels after a day or two of price rebounding.

Analysis

We are approaching extreme levels of fear, indicating that the current sell-off is likely to be overextended and we may see a short-term price bottom sometime soon.

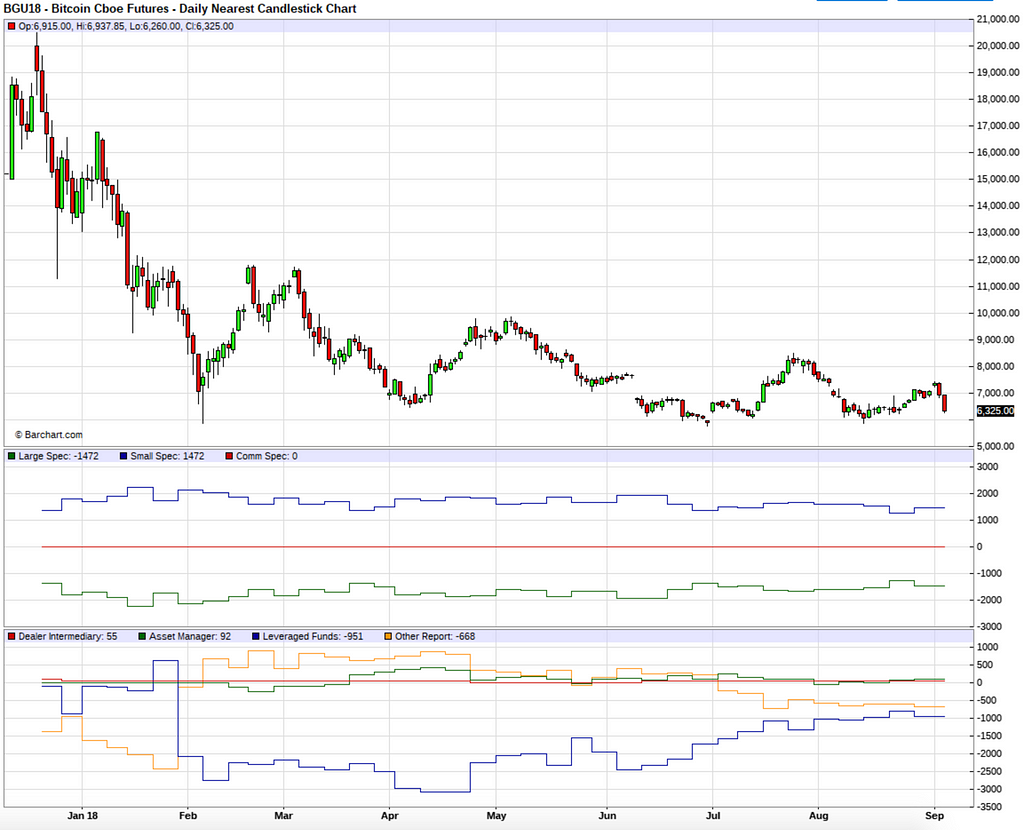

CBOE Futures Commitment of Traders

Why it makes sense

The CFTC publishes a weekly report breaking down positions held in various futures markets by category of holder — large speculators, small speculators, and commercial hedgers. This report is called the Commitment of Traders. Since BTC has several listed futures contracts now, we can see this data. CBOE’s Bitcoin COT data is used.

Some traders like to use this data in order to identify the aggregate position of small speculators. These players are generally considered to be the “dumb money” and it can be profitable to take the opposite position from them.

Source: barchart.com

Source: barchart.com

Why it doesn’t

Futures trading, while growing, is still a minority of US Bitcoin trading volume. As a result, these positions represent relatively small exposure. Also, we can see that they don’t tend to matter that much and aren’t historically very correlated with price changes. Finally, Bitcoin’s strange market structure — with no real commercial hedging activity (theoretically, this should be miners but in practice doesn’t really exist), and few mechanisms to short the spot market, may make this analysis less effective.

Analysis

Small speculators have been net long since the creation of this market, which is perhaps predictive of further downside in BTC prices. Relative to the historical range of the small spec position, we are currently near the middle which may indicate reduced bullishness on their part.

Valuation Summary

With any valuation methodology, there is always the danger of optimizing for what has worked historically — markets are dynamics and so signals tend to get weaker over time as more and more of the market utilizes them.

In general, it should be remembered that we are in the Stone Age for valuation tools for crypto assets and so all valuation models (or collection of models as we’ve presented here) should be taken with a large grain of salt and viewed skeptically.

Having said that, nearly all our indicators suggest that the bear market of 2018 will continue for the next few months.

2. Technology

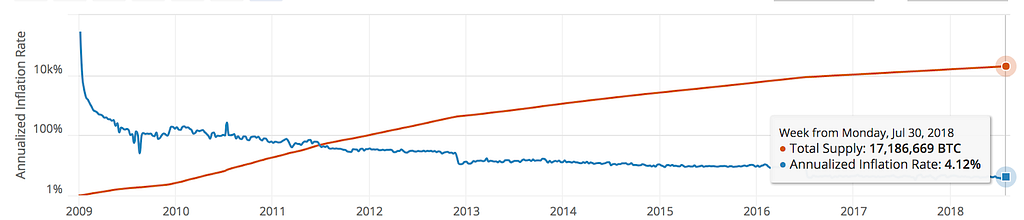

Total Bitcoin Supply

As of July 30, 2018, 17.186 million of 21 million bitcoin (81.8% of final supply) have been issued. The current block reward for miners is 12.5 bitcoin with the next halving to 6.25 bitcoin scheduled for 2020. At the current block reward, annual inflation of Bitcoin is 4.12%.

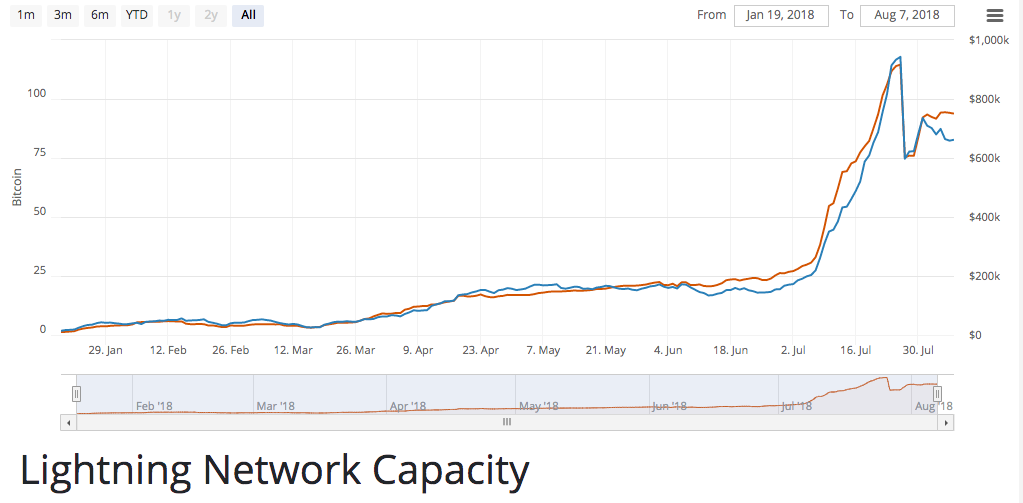

Lightning

Lightning capacity has been steadily growing this year but is still in just-a-toy phase, with capacity still not having reached a million dollars.

The most popular lightning apps are Satoshi’s place, a digital graffiti wall where rewriting a pixel costs 1 satoshi, and Lightning Spin, a gambling app. (See a full list of lightning apps).

Setting up a lightning node (Compiling, installing, and running Lightning Network Daemon, lnd) is fairly straightforward for any developer with a basic knowledge of bitcoin and the documentation seems to be quite good. However, maintaining a lightning node as a payment hub is difficult and not profitable. In a test, a lightning node routed 260 payments for other users, averaged a profit of $0.0012 USD per transaction. There is a lot of room for optimizing those fees, but it remains to be seen if the economic incentives exist to run lightning nodes (i.e. Is it a good business?)

Sending payments to buy goods and services using Lightning is indeed cheaper than using the base layer Bitcoin blockchain, but routing errors and wallet bugs make it currently impractical even for technical users.

There is lots of research and development activity happening on lightning. Notably Alex Bosworth has been working on submarine swaps which allow users to use on-chain tokens to pay for Lightning invoice payments. This allows someone to pay a lightning invoice — make a payment to someone, e.g. a friend or merchant — without having to setup their own lightning wallet by leveraging a cross-chain transaction with other protocols, like Dash or Litecoin.

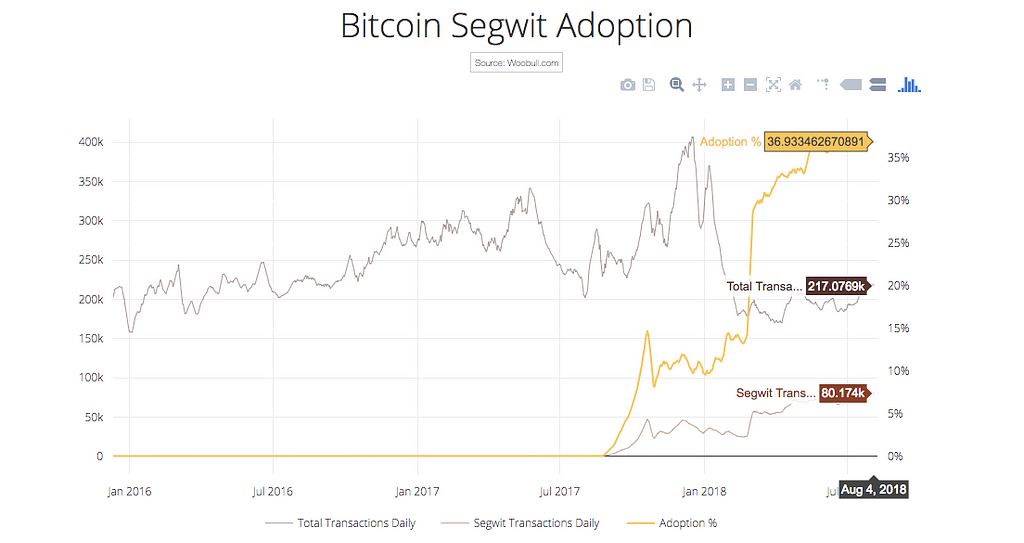

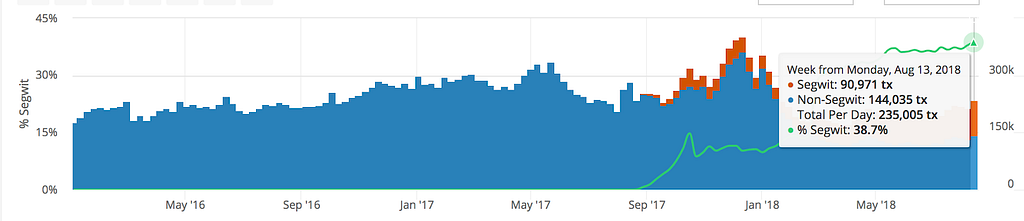

SegWit Adoption

SegWit (short for Segregated Witness) is a protocol upgrade that changes the way blockchain data is stored. Segwit was initially intended to fix a Bitcoin limitation known as malleability which prevented the development of more complex features such as second-layer protocols (like lightning) and smart contracts. A side benefit of SegWit was that it reduced the size of transactions so that the Bitcoin blockchain could accomodate more transactions per second without increasing transaction fees.

As of early August, SegWit adoption is at almost 40%.

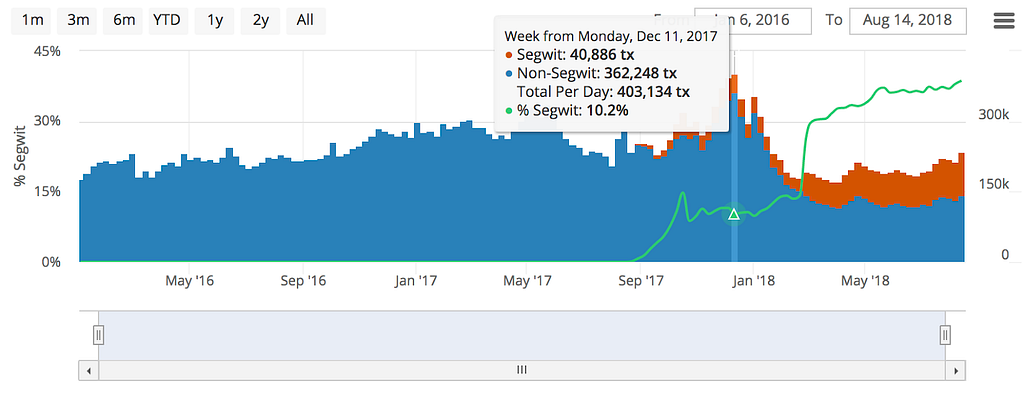

The total number of Bitcoin transactions per day peaked on Dec 11, 2017 at 403,134 transactions.

As of August 13, the network is processing 235,000 transactions per day, about the same level it was at in October of 2016.

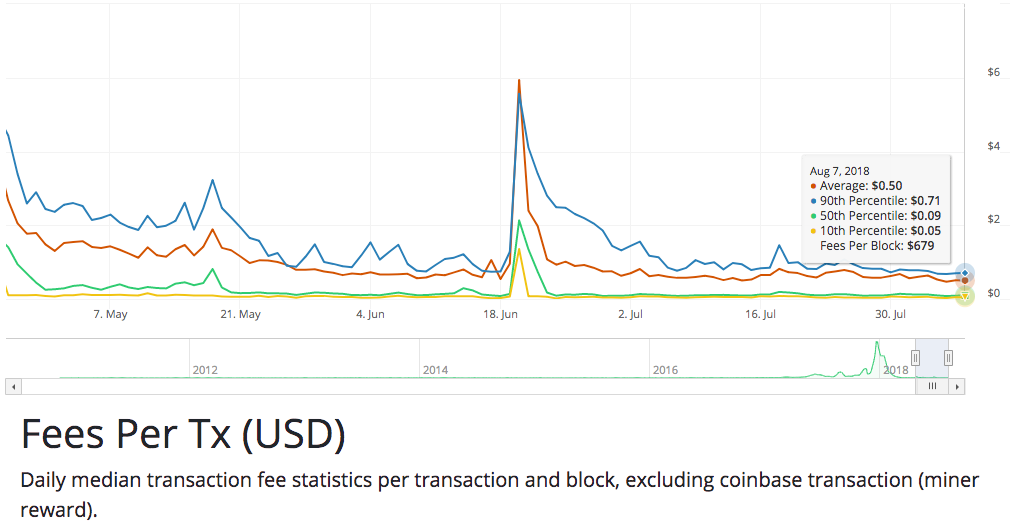

Transaction Fees

Combined with decreased network usage, average transaction fees have gone from a high of $50 in December to $0.50. Median fees have fallen from $30.86 to $0.09.

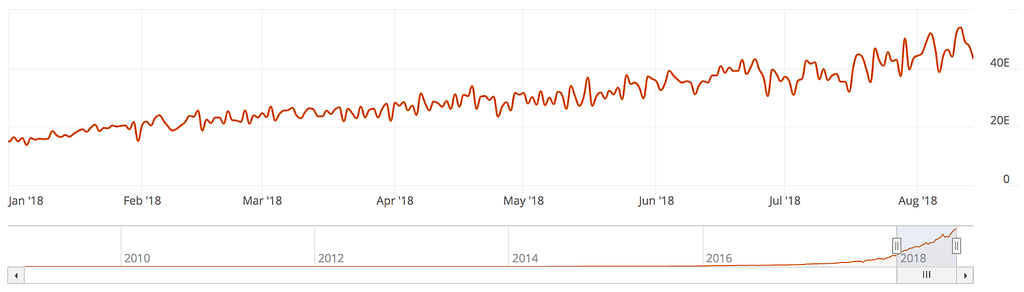

Hashrate

Even as price has fallen, hashrate has increased dramatically from 15 Terahashes/second on January 1, 2018 to 54 Terahashes/second on August 11, 2018.

Historically, Bitcoin hashrate has grown at a rate of about 300% per year. We’ve already seen that growth as of August in 2018 despite the drop in price.

This is good for Bitcoin’s security. As of mid-2018, it would cost around ten billion dollars to buy enough computers and electricity to mount a 51% attack. This limits viable attackers to a fairly small group of nation states and major corporations.

Unless Bitcoin’s price rebounds quickly, it likely means many of the miners which jumped in after seeing the appreciation in 2017 will become unprofitable.

Estimates vary as to what the exact break even price is for Bitcoin mining, but at this point, I wouldn’t even look into it unless you’re getting electricity at rates below $0.05/kwh. Only a few places in the United States have electricity at this rate.

Technology Summary

Bitcoin is unique among cryptoassets because there isn’t a whole lot that needs to get done technologically to make it viable as a form of digital gold over the next five to ten years.

Even with transaction fees in the tens of dollars, it can still serve as a sovereign-level censorship-resistant store of wealth. Current markets which exist largely because of their censorship resistant properties include the gold market (est. $6 trillion) and the offshore banking industry (est. $20 trillion).

That said, Segwit adoption is up meaningfully which, along with decreased network activity, has brought median transaction fees down under USD $0.10.

Hashrate, an important measure of Bitcoin’s security and censorship resistance is up over 300% YTD.

The Lightning Network is the most talked about technical development on Bitcoin right now but it is probably near the peak of the Gartner hype cycle. There is lots of talk about what can be done with it, but we are probably still at least a couple of years from seeing meaningful adoption.

Long term concerns around fungibility (because of Bitcoin’s limited privacy and pseudonymity rather than anonymity making it possible some coins will be considered “tainted”) and stability of Bitcoin in a future without the mining reward are real but don’t seem like short-term concerns.

Want to read more of this report later?

Click here to download a beautifully formatted PDF version.

3. Regulation / Legal

Bitcoin is still a commodity

In 2015, the CFTC ruled that Bitcoin was a commodity and would be regulated under their purview. In March this year, U.S. District Judge Jack Weinstein upheld that the CFTC statement, saying it was supported by the plain meaning of the word “commodity” and that the CFTC had broad leeway to interpret the federal law regulating commodities.

This is nice because it means Bitcoin face the least regulatory uncertainty of all the cryptoassets.

SEC rejects Winklevoss Bitcoin ETF

The Winklevii proposed an ETF that would hold spot BTC bought via Gemini with each share worth .01 BTC. The proposal was rejected by the SEC primarily because they believed the underlying spot market had too much room for manipulation.

This was in meaningful part because the market would be entirely dependent on the Gemini exchange’s market rather than a broader one. Using a market with more volume and liquidity might have altered the ruling.

Regulatory Arbitrage Will Continue

Binance made headlines when the exchange shifted to Malta due to rising regulatory requirements. Malta has used the opportunity to attract more blockchain startups. As regulatory environments around the world continue to fail to provide clarity on how Bitcoin and other crypto assets will be treated, both capital and entrepreneurs are likely to continue moving to friendlier jurisdictions to avoid rising scrutiny.

Zug, Switzerland has historically been the home to many crypto projects and Gibraltar appears to be opening up. Despite the regulatory progress and favorableness of these jurisdictions, it will take a larger market like the UK or U.S. to clarify their regulatory stance betwore many large institutions are willing to get involved.

International Regulatory Bodies Remain Fairly Neutral

Though some of the Bitcoin faithful believe that Bitcoin is poised to become a reserve asset, the international regulatory bodies don’t seem too concerned about that happening anytime soon.

The G20’s Financial Stability Board said in March of 2018 that they didn’t believe Bitcoin and other cryptoassets posed a threat to the stability of global markets.

The IMF also seems neutral with Managing Director Christine Lagarde pushing for an even-handed regulatory approach that balances protecting investors with allowing innovation.

Regulation Summary

Bitcoin is the most regulatory black/white of the cryptoassets and despite ETF rejections and some companies in the space engaging in regulatory arbitrage, seems to have pretty favorable regulatory tailwinds.

4. Ways of Getting Exposure

Overview:

For the investor considering how to get exposure, we divided the vehicles into three buckets:

- Non-custodial, Publicly Listed Options available through a traditional brokerage account

- Non-custodial options restricted to accredited investors and high net worth individuals

- Personal custody options

Publicly Listed Options

Closed End Funds

Many institutions will want to hold crypto exposure through a publicly-listed vehicle with relatively low fees: an exchange-traded fund or closed-end fund like Grayscale’s Bitcoin Investment Trust. Grayscale’s GBTC is one of the few available options, but fees could ideally be lower (currently at 2%). A bigger problem is it trades at a very high premium to NAV, about 50% as of July 2018, though it has traded as high as a 100% premium. We expect that premium to drop as more competition comes into the market like Coinshares’ recently-listed Bitcoin ETN.

Pros

- Publicly traded on stock exchanges

Cons

- Fees

- Trading at large premium to NAV

Who It’s Right For:

People who want to invest using assets in their IRA/401k and institutions that want to offer it to clients but don’t have a trusted custody solutions. (Hence the premium — it’s the only way for these market segments to get exposure.) In general, if you can avoid paying a premium (avoid GBTC for now, try the Coinshares product) then this is a relatively easy-to-access vehicle that is already available.

ETFs

The SEC recently postponed ruling on five Bitcoin-related exchange-traded funds until September and most sources I’ve spoken with put the odds of approval at 10–15%. Atlantis Asset Management chief investment strategist Michael Cohn said an approval would mean “they’re putting a rubber stamp on [Bitcoin] as an asset, and I don’t think governments want to go there yet.”

So ETFs are still not an option though the momentum is there and it seems likely that one will be approved within the next 12 months. As mentioned above, Coinshares did successfuly list a Bitcoin ETN.

Pros

- Publicly traded instrument that is familiar

- Will tend to trade closer to NAV than a CEF

Cons

- Does not yet exist or is more difficult to purchase (The Coinshares ETN have residency restrictions similar to offshore mutual funds. This is not something which some brokerages such as Schwab are prepared to monitor)

- In some ways, bitcoin’s volatility makes it more appropriate for active management so an ETF might not be the best vehicle.

- You don’t have custody. It’s possible that the custodian could be compromised, in which case it seems likely the losses would fall ot the holders of the ETF.

Who It’s Right For:

The same parties interested in CEFs, with slightly broader interest as a result of the improved pricing that comes with a ETF vs CEF structure.

Publicly Listed Miners and Chip Manufacturers

Some of the Bitcoin mining companies are publicly traded and investing in them is one way to get exposure to Bitcoin. Also in this camp are the chip manufacturers.

Publicly Listed Miners include:

- 360 Blockchain (CSE:CODE)

- DMG Blockchain (TSXV:DMGI)

- HashChain Technology (TSXV:KASH)

- HIVE Blockchain (TSXV:HIVE)

- Neptune Dash (TSXV:DASH)

Publicly Listed Chip Manufacturers include:

In the U.S.

- NVIDIA

- AMD

- Micron

In Asia

- TSMC

- GUC

- JCET

- MediaTek

- Nanya Tech

Pros

- Publicly traded

Cons

- You’re making a bet on the profitability of a specific company’s mining operation. The stock price may be weakly correlated with BTC price. It’s entirely possible for Bitcoin to appreciate and for all these company’s stock prices to fall.

- This is likely doubly true right now as all signs point to it being a bad time to get in mining business. Given hashpower increases noted above, will need to say major price appreciation in BTC for most miners to stay profitable. If mining growth stops or reverses, that will be felt all the way through the supply chain here.

Who It’s Right For:

Likely a good bet for someone that has done a deep analysis of the specific mining operation and is interested in making a bit on their ability to continue to profit in such a competitive space.

For Accredited Investors and HNWIs

Bitwise (and other low-fee, long-only funds)

While ETFs are not available, a number of funds have popped up trying to serve an ETF-like purpose for accredited investors.

Bitwise is the most well-known of a swath of index funds that have popped up in the last 12 months. Bitwise primary (and currently only) product is the Bitwise HOLD 10, a basket of the 10 largest coins which represent 80% of the market and is rebalanced monthly.

Competitors

- Crescent Crypto

- Pantera’s Bitcoin fund

Pros

- Direct exposure to coins

- Indexing lets you place a bet on the whole space without needing a specific thesis

- Non-custodial (depending on how you look at it)

- No performance fee

- Weekly liquidity (depending on how you look at it — a lot can happen in a week in crypto)

Cons

- Non-custodial (could be a pro, depending on how you look at it)

- For the first 12 months, redemptions incur a 3% early withdrawal fee. After 12 months, there is no fee to withdraw.

- Exposure to “shitcoins” (e.g. XRP) and risk they carry (regulatory and otherwise)

Actively Managed Hedge Funds

Pros

- Potential to profit from volatility with active management

Cons

- Most don’t know what they are doing for operational security

- High performance fees

- Long lockups

Who It’s Right For:

The investor looking to take advantage of the market’s immaturity to get alpha as well as get exposure to the space. Given the immaturity of crypto markets, active management makes quite a lot of sense to us.

Institutional Custody

There are a number of institutional custody solutions popping up including Coinbase Custody, Northern Trust, and Goldman which offers custody through a regulated, institutional broker-dealer.

Pros

- Cold Storage

Cons

- Monthly Liquidity

Personal Custody

Coinbase and other exchanges

The easiest and most common way for individuals to buy bitcoin is through an exchange (Coinbase being the most popular in the U.S. — though others including Square, Circle Robinhood, and Gemini are gaining market share.)

Pros

- Best User Experience

- Probably have better security and custody than someone with very little knowledge trying to do self-custody

Cons

- “Not your keys not your bitcoin” — these are bearer instruments so there is much more risk than leaving stocks with a custodian.

- More and more problems reported withdrawing funds in recent months (anecdotal)

Who It’s Right For:

Retail investors who don’t know a lot about the space but want to “throw $100 at it so I have some skin in the game to learn about it.”

Hardware Wallet

You can buy bitcoin on an exchange using fiat and transfer it to your hardware wallet. Hardware wallets are the most secure option for storing bitcoin. The hardware wallet (basically a snazzy looking USB stick) acts a form of 2 Factor authentication. In order to steal your bitcoin, a hacker would need to get your password and physical possession of the device. Since most Bitcoin thefts have are purely virtual, having a physical component dramatically increases the security.

Pros

- “Not your keys not your bitcoin” — You have full control over the Bitcoin.

- Hard to hack virtually

Cons

- You need good procedures around recovery seed storage

- Easier to lose your bitcoin

Who It’s Right For:

More technically sophisticated retail investor who has some basic knowledge of operational security.

Ways of Getting Exposure: Summary

Publicly listed options are still limited and what options there are have significant drawbacks. It seems likely this will change over the next 12 months, though probably not over the next three.

Following the 2017 boom, a handful of non-custodial new options exist for accredited investors and HNWI exist and generally good though investors are forced to choose between low fees and very little customization (cap weighted index funds) or high fees and more customization (actively managed funds).

Personal custody options have not changed much over the last couple of years, perhaps because the options available are generally seen as being pretty good. For individuals institutions choosing to self-custody, a working understanding of operational security is critical.

Want to get future reports delivered to your inbox?

Something we missed, that you would like to see us include? Disagree or have feedback? Let us know on Twitter (Taylor and Gary) or email

Disclosure: This is not financial advice. We are long Bitcoin.

State of Bitcoin (Fall 2018) was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.