Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Original art is by Borbay. A bit modified to my taste.

Original art is by Borbay. A bit modified to my taste.Securitization and Tokenization: Two Sides of the Same Coin?

It occurs that there’s so many evidence that history is a non-stoping spinning of the various ideas. It’s like a spinning circle of denying each other’s ideas, that first emerge, then being negated and to finally uprise in a brand-new dialectic way. May Thou forgive me for my little worshiping to Hegel.

The starting point of this short oeuvre was that kind of wonder that I had when watching “The Big Short” for the n-th time in life. As it seemed to me, the main lever that led to the Economic Crisis of 2007 (described in the movie) — namely, the securitization of assets, — and the tokenization of assets that I saw every time I look around the “next-gen blockchain and crypto project’s” whitepaper, are indeed the same process of pouring the liquidity into everything, thus actualizing the neoliberal project. Leaving alone the left-like critique of this, I managed to clarify the differences between the two and find out if there’s something missing in my understanding.

Let’s go.

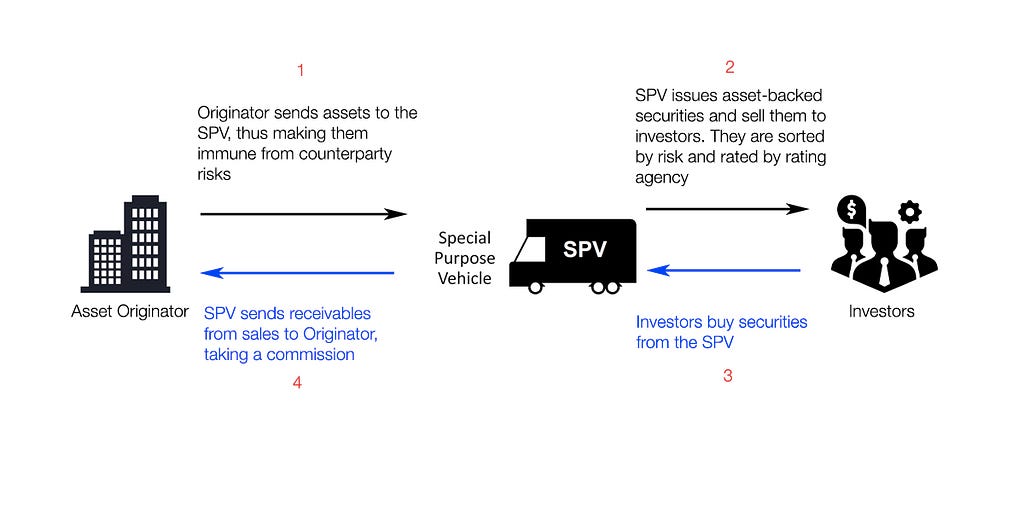

Securitization is basically a practice of pooling different types of low liquid assets that generate separate cash flows (like mortgages, auto loans or credit card debt obligations) and selling their aggregated cash flow (in some rating-based portions) to third-party investors as securities, i.e. tradable financial asset. Although the history of this practice roots back to the 18th century, it’s a common thing to talk about securitization starting from 70–80s, when the practice was revitalized and given a new life by Wall Street traders. More on that one can find in a great book by Michael Lewis.

It would be an exaggeration to say that one single person created securitization. However, there are many people saying that Lewis Ranieri is the father of practice.

BusinessWeek said that with the creation of mortgage-backed securities, “Ranieri’s job was to sell those bonds — at a time when only 15 states recognized MBS as legal investments. With a trader’s nerve and a salesman’s persuasiveness, he did much more, creating the market to trade MBS and winning Washington lobbying battles to remove legal and tax barriers.”

All in all, securitization is about repackaging mortgages and other assets and making very liquid and attractive financial instruments. The process of securitization looks as described in this picture [simplified]:

Before the 2008 crisis, combining home loans and selling them to investors was a very profitable business for banks. The cause of the crisis was the inability of many borrowers to repay the debt (mainly subprime mortgages, the ones that are of very high risk), it undermined the securitization market and caused losses in the trillions of dollars. Generally speaking, it was a triumph of greed — hungry bankers sold so many high-risk mortgages, investment banks mixed them up with low-risk mortgages, thus making a “relatively” stable product, rating agencies pretended everything is ALRIGHT and assigned AAA ratings to these products, and so on and so on.

Human nature.

In 2018, eleven years later from the Financial Crisis, global structured finance issuance increased by about 18% yearly over to approximately $500 billion during the first half of 2018. The U.S., China, and Europe all recorded considerable growth, while Australia and Latin America experienced declines. In their report, experts foresaw that the growth will continue to approximately $1 trillion of global securitization by year-end 2018.

Nowadays, Credit Suisse Group AG, U.S. Bancorp, Wells Fargo & Co. and many more are testing the distributed ledger technology and blockchain as ways to facilitate tracking securitization of assets. Deloitte claims that “blockchain, along with smart contracts, promises to transform many activities in the securitization lifecycle”.

A Little of Likbez

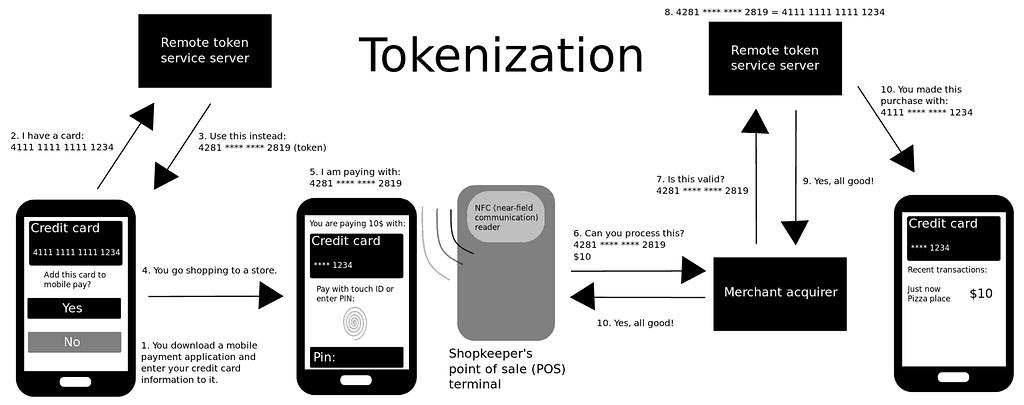

This is a simplified example of how mobile payment tokenization commonly works via a mobile phone application with a credit card. (Wikipedia)

This is a simplified example of how mobile payment tokenization commonly works via a mobile phone application with a credit card. (Wikipedia)

Initially, tokenization was used to describe a process when a sensitive data element is substituted with a non-sensitive equivalent, referred to as a token, that has no extrinsic or exploitable meaning or value. Thus being said, tokenization is a process similar to encryption, though not exactly. In a sense, it’s more like public and private keys — where private one is a sensitive data element, and the public one is a token. Example — in accordance with PCI Council, an information security standard obligatory for all credit and debit card providers, payment card number (PAN) which includes personal information of the cardholder, must be tokenized and replaced with a surrogate value called a token. Then this token is used when transacting and etc.

With the advent of blockchain and cryptocurrencies, tokenization got a broader meaning. According to Strategy&, asset tokenization describes the process of converting assets into digital tokens on a blockchain. Under potential assets for tokenization, the list:

- Fiat currencies (described in one of the past articles);

- Commodities;

- Real estate;

- Art and collectibles and more.

And so what?

The difference with the past notion of tokenization is clear: while tokenized PAN in the example above doesn’t have an intrinsic value, it cannot be traded. Instead, tokenized with ERC-20 Ethereum-compatible blockchain house, mortgage, business, and other stuff can be easily traded once listed on the exchange. Yes for sure there is a number of legal obstacles, but the possibility is already created.

Brave new world

What is particularly intriguing me in this surge for liquid, tradeable and tokenized world is this: the assets around us and even our time (just think for a while about digital advertising and the time you spend on Facebook and Instagram) are becoming constantly bought and sold, I believe there will emerge even more marketplace (like OLX or Avito, but with a much broader functionality) that allows trading automatically everything, from things to time spent with other people, let alone other types of tradeable things that I cannot or don’t want to imagine (dark market).

I believe that the programmability of tokens (that becomes possibles with smart contracts) opens up a way to a totally liquid world. Various combinations of assets (as long as everything becomes asset) can be sorted, grouped and sold in the most efficient way (Nash equilibrium). The only thing that cannot be solved here is risks so risk management specialists and game theory graduates (tokenomics) will be of high demand in the future.

With all the arising concerns, I believe that a sort of Basic Income must be enacted, as the coming situation is designed to stimulate global inequality. What if this basic income for every single person would be formed out of his or her real estate property, savings, taxes, estimated free content consumed (you won’t have to pay for Netflix anymore!) and so on, tokenized and grouped into a General-Backed-Security (GBS), and sold to a group of high-income individuals as a bond? What if there would be a data breach or people default on their debts? Debts for free content supposed to be consumed within the next 10 year?

So many questions, so few answers.

The opinion of the author may not coincide with his point of view.

For personal inquiries, please text in Telegram.

On Securitization and Tokenization: Two Sides of the Same Coin? was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.