Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

By Standard Kepler Research

This is 1/2 for the series of Central Bank Digital Currencies by Standard Kepler Research

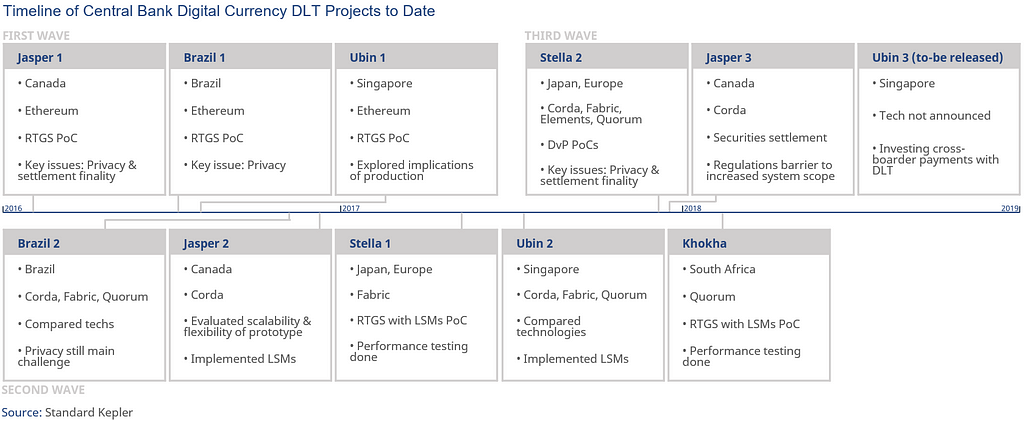

figure 1, Timeline of Central Bank Digital Currency Projects

figure 1, Timeline of Central Bank Digital Currency Projects

INTRODUCTION

We have previously identified Central Bank Digital Currencies (CBDC) as one of the more promising potential applications of Distributed Ledger Technology (DLT). As is made evident in Figure 1, a number of CBDC projects have been launched for purposes of evaluating the suitability of blockchain in future payment systems. Financial market infrastructures (FMIs) are critically important institutions responsible for providing clearing, settlement and the recording of financial transactions. FMIs are trusted third parties between financial institutions, using centralized ledgers to record and track transactions. FMI operators display significant interest in technology that may increase the efficiency of FMIs, and three key waves of exploratory CBDC DLT projects have been launched to date. A number of benefits are typically hypothesised for such future payment systems. It is speculated that financial sector back-office costs can be reduced via increased settlement automation. Further advantages are expected with regards to reliability and traceability of information, as well as shorter settlement times. However, CBDC DLT projects to date indicate that the technology is currently lacking the maturity to achieve these improvements.

Due to their critical importance to financial stability, FMIs balance a number of significant risks. These include governance and legal risks, credit and liquidity risks, settlement risk, and operational risk. Appropriate transparency and privacy for system participants must also be achieved while maintaining the benefits of DLT technology. This results in a series of trade-offs, significantly so between system privacy, resilience, and scalability. Existing CBDC projects indicate that Corda achieves privacy and scalability at the cost of resilience, Hyperledger Fabric achieves privacy at the cost of resilience and privacy, and Quorum’s zero-knowledge proofs achieve privacy at the cost of scalability. CBDC DLT projects should be studied closely, as they bring us closer to identifying the core value proposition of DLT. We will make efforts to update this foundational report as further developments occur in the space of Central Bank Digital Currencies.

RETAIL PAYMENT SYSTEMS

WHAT IS MONEY?

The term crypto-currencies implies similarities with established currencies issued by central banks. This in turn leads to the question of whether crypto-currencies should be regarded as money. The world’s oldest central bank (the Swedish Riksbank) is keen to stress that “theories of money and how to create a functioning monetary system can be understood on the basis of concrete problems that society has attempted to resolve throughout history”. There are different definitions of money in existence, with modern definitions having developed to solve many of the pain-points involved in previous systems of barter exchange.

Metallism

Ties money to the value of an underlying good. These goods have often been metals, hence the name. A core idea of Metallism is that the limited supply of metals, and the increasing cost of excavating more, act as natural inflation limits. Bitcoin has found inspiration in Metallism, incorporating similar but digital limits to the total Bitcoin supply.

Chartalism

Is another theory for how to define money. According to Chartalism, the value of money is derived from its status as legal tender issued by a national state. Chartalism thus places an indirect responsibility with the state for maintaining a functioning monetary system.

Functionalism

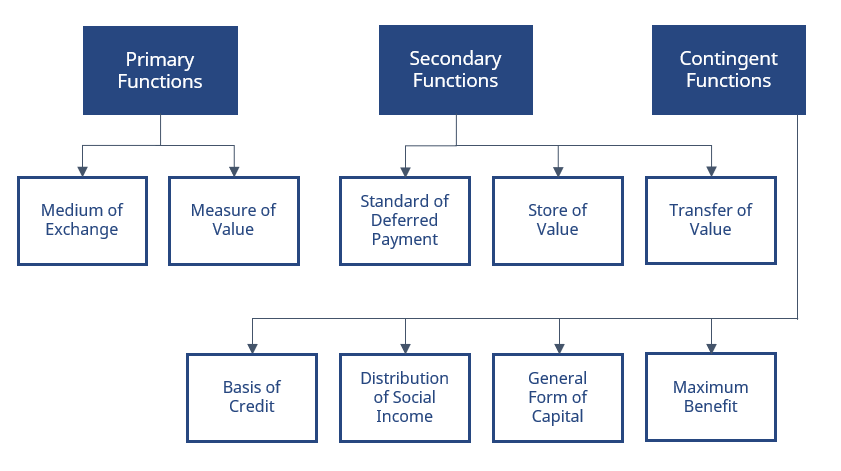

The dominant modern interpretation of money, builds further on Chartalism. According to Functionalism, money must fulfil three criteria of functionality in order to be considered money. Money must function as 1) a means of payment, 2) a unit of account, and 3) a store of value. Means of payment means that money can realistically be used to pay a seller in return for goods, so as to avoid having to repay the seller using goods or services.

To function as a means of payment means that money must function as a recognized measurement of value for different goods and services in the economy. Finally, to work as a store of value money should provide price stability, and peoples’ decision to spend or not spend money should not be influenced by volatility in the value of money.

See Figure 2 for more details on the expected functionality of modern money.

Central banks are typically responsible for ensuring that money can these three core functions. An example is found in the inflation targets often set by central banks, with the goal of maintaining the storage of value functionality of money. It is the opinion of several central banks that crypto-currencies should not be considered money, and most crypto-currencies are neither tied to the value of a tradeable good nor are they issued by national states.

Cryptocurrencies further struggle to fulfil some of the criteria associated to Functionalism, for instance: it must be easy to ascertain the value of money, money must be widely accepted in payments, and money must be durable and exhibit price stability.

figure 2

figure 2

This is not to say that cryptocurrencies cannot be issued by national states (some have been) or that they cannot be tied to the value of physical goods (some have been). But in order for crypto to see mass adoption as retail payment tools they must fulfil the criteria of Functionalism, and the path towards achieving price stability, sufficient price transparency, and wide recognition of crypto among buyers and sellers is long and difficult.

It is made more difficult by the fact that the primary interest in crypto-currencies has been for speculative purposes, not for purposes of conducting transactions. It is further unlikely that central banks would recognize money (crypto-currencies) over which central banks lack the central authority to make monetary decisions (e.g. adjusting supply).

Central Bank Digital Currencies (CBDC), for the purposes of establishing retail payment systems, enter the picture as noteworthy alternatives to the likes of Bitcoin and Bitcoin Cash. Proposed retail CBDCs would not only have the potential to fulfill the criteria of Functionalism, but are also poised to solve some further issues that exist in modern economies, including an over-reliance on private providers and owners of retail payment infrastructure.

RETAIL PAYMENT SYSTEMS AND DLT

CBDC driven Retail Payment Systems (RPS) have been proposed as solutions to a number of problems. Some of these problems are related to the costs of using cash, and some are related to a lack of cash. Note that CBDC RPS can be designed without DLT, and DLT is just one possible underlying database infrastructure for such systems.

In scenario A, some countries have considered CBDC RPS as a way to reduce the usage of cash. The goal being to reduce the financial and environmental costs associated with handling cash, as well as the black economies which are facilitated by cash. In scenario B, countries such as Sweden have in recent years seen drastic reductions in cash usage.

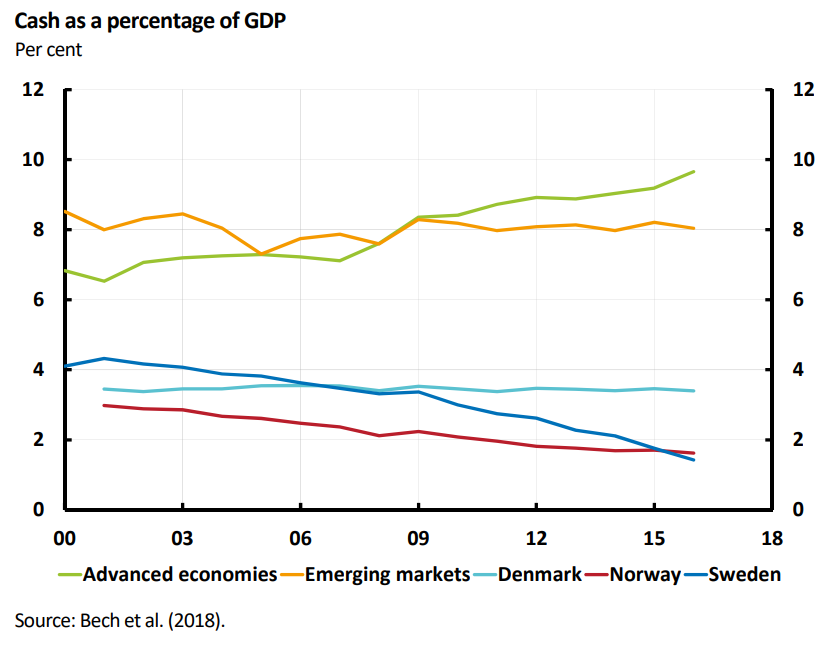

Cash currently constitutes just over 1% of GDP in Sweden, compared to the European average of 10% of GDP (see Figure 3). Half of Swedish retailers further expect they will stop accepting cash by 2025 at the latest. Central banks fear that such reductions in cash usage and cash supply can lead to difficulties for the public to gain access to central bank risk-free money and increased consolidation in the financial infrastructure among private digital retail payment systems.

This in turn could lead to a more inefficient and vulnerable payment market, with decreased trust in the monetary payment system.

figure 3, Graph Source: The Swedish Central Bank, E-krona project 1

figure 3, Graph Source: The Swedish Central Bank, E-krona project 1

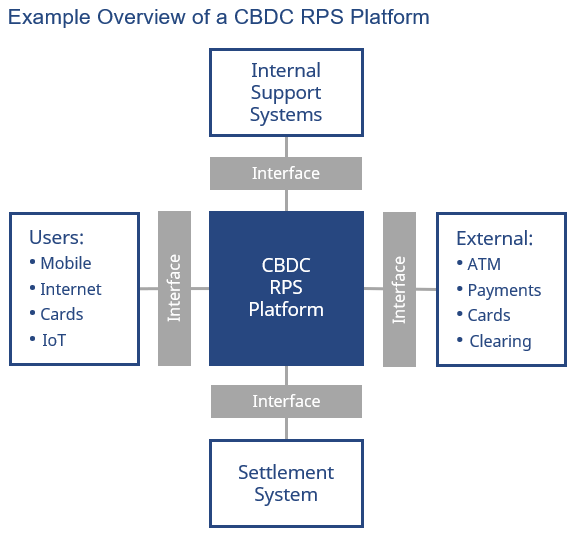

CBDC RPS are conceived as a solution to the above two scenarios. A “digital dollar” platform could allow the public to hold digital dollars issued and guaranteed by the central bank. The platform would interface with users (via internet, card, IoT, etc.), settlement systems, internal support systems, and external systems such as ATM companies and payment service providers (see Figure 4).

figure 4

figure 4

The costs associated with such digital dollars would likely be small in comparison to the handling costs of physical dollars, and digital dollars could provide central banks with traceability to limit black markets. Digital dollars would also provide the public with a guaranteed RPS that (unlike most existing RPS) is not run by private actors.

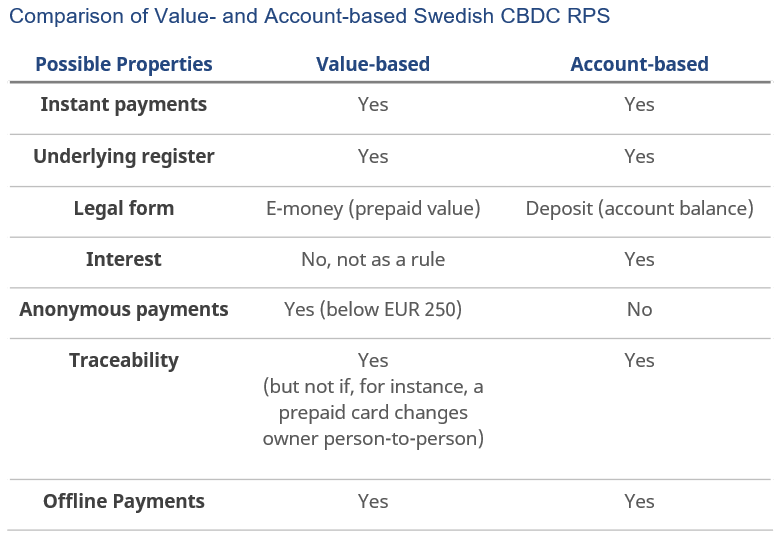

There are two primary approaches towards designing a CBDC RPS. It may be account-based (held in an account with the central bank) or value-based (stored in an app or on a card). Both require an underlying register that keeps track of transactions and ownership, meaning that usage is traceable. DLT has been considers as a possible choice, but “from a purely technical point of view, [the Swedish Central Bank] can see nothing at this point in time that would prevent an e-krona solution built around a central register.”

Expect CBDC RPS to attract more attention in the future, although primarily in niche markets where cash usage is low (most countries still see significant cash usage, a notable example being the USA), or where there are significant black markets in existence. There are still important decisions to make in the design of an RPS:

Should the digital dollar carry interest? Should it be account or value-based?

A digital dollar could make bank runs easier. Is such ease desirable or not? Strong demand for digital dollars (especially interest-bearing dollars) could also drain commercial banks, leading to a reduced ability to issue credit. These decisions would result in a new set of potential risks to the financial system that have to be carefully evaluated.

For now, a value-based non-interest bearing dollar seems to be the most likely proof-of-concept candidate. To quote a Deutsche Bank report from 2018, “a compelling reason for consumers to switch voluntarily to crypto euros is hard to see — at least for the time being.”

figure 5

figure 5

WHOLESALE PAYMENT SYSTEMS

WHOLESALE PAYMENT SYSTEMS AND DLT CBDC

Wholesale Payment Systems (WPS) have seen wider and more rapid prototyping than CBDC Retail Payment Systems (RTS). This likely due to the more significant cost savings that may be possible via CBDC WPS. Furthermore, the interests of private financial institutions and central banks are generally aligned in the development of CBDC WPS, while CBDC RTS are viewed as possible competitors to existing RTS operated by private financial institutions.

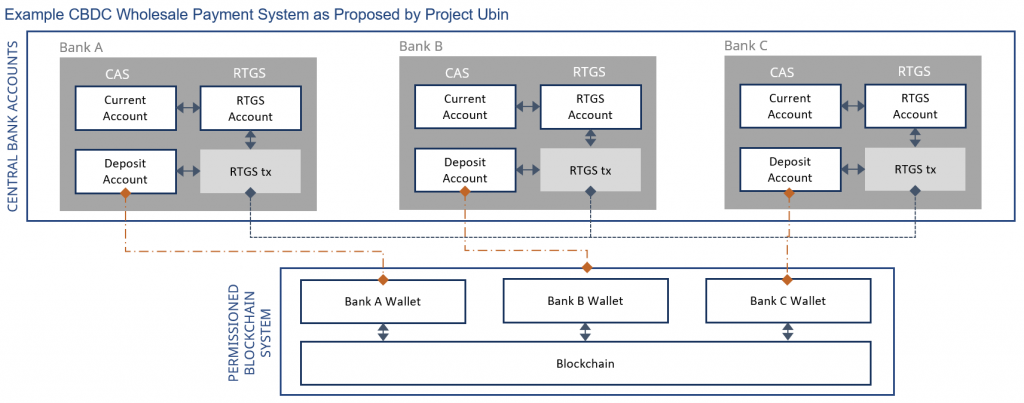

A wholesale payment system “deals with inter-bank, inter-country large value, large volume real-time payments and related clearing and settlement systems governed by central banks integrating various globally accepted standards.” A CBDC WPS considers how digital currencies can be utilized to improve the efficiency of WPS. A simplified example implementation of a WPS is proposed in Project Ubin, and is outlined in Figure6.

In this proposed system, banks hold a special deposit account with the central bank. A bank can deposit funds into this deposit account from the bank’s RTGS account. The balance of this deposit is mirrored in a digital currency wallet on the permissioned blockchain system. Moving funds into the deposit account thus creates digital currency (in this case Deposit Receipts) in the wallet, and withdrawals from the Deposit Account burns Deposit Receipts in the wallet. Banks, with Deposit Accounts, can then transfer Deposits Receipts between bank wallets on the blockchain.

figure 6, example CBDC wholesale payment system as proposed by project Ubin

figure 6, example CBDC wholesale payment system as proposed by project Ubin

Such a system can be designed around DLT, and the specifics of the system depends on the digital ledger technology chosen. The options most commonly considered are R3’s Corda, Hyperledger’s Fabric, and JP Morgan’s Quorum, which are going to be introduced introduced in the coming part.

Several WPS proof-of-concepts have been developed to date. The concepts tested in these projects using these systems have generally proven that DLT is able to execute transactions at a rate matching existing RTGS volumes and with finality, albeit often at the cost of limited privacy or system resilience. Further development would be needed to achieve more efficient trade-offs between these aspects.

One must also note that a full-fledged CBDC WPS ought to include liquidity management and credit extension functionality. Concepts for both of these functions exist, but are considered beyond the scope of this introduction on the CBDC topic.

As more actors in financial markets consider introducing DLT based systems, the complexity of interoperability and the potential for new business models both increase.

Originally published at https://www.standardkepler.com on January 21, 2019.

Standard Kepler is Asia’s leading blockchain financial services provider, offering market changing research insights, in addition to holistic advisory, crypto trading, and custodian services. We take great pride in being able to offer professional services that are trusted for our honesty and driven by technology. Headquartered in Hong Kong, Standard Kepler’s management team previously served in JP Morgan, Macquarie Capital, State Street, and KPMG.

REFERENCES

Bank of Canada; Payments Canada; R3. 2017. Project Jasper: Outline.

Bank of Canada; Payments Canada; R3. 2017. Project Jasper: A Canadian Experiment with DLT for Domestic Interbank Payments Settlement.

Bank of Canada. 2018. Project Jasper: Are distributed wholesale payment systems feasible yet?

Bank of Canada; TMX Group; Payments Canada; Accenture; R3. 2018. Jasper Phase 3: Securities settlement using DLT.

Corda. 2018. The Corda Platform: An Introduction.

Deutsche Bank Research. 2018. Why would we use crypto euros?

European Central Bank. 2018. Stella: BOJ/ECB joint research project on DLT.

Hyperledger. 2018. An Introduction to Hyperledger.

JP Morgan. Quorum Whitepaper.

Monetary Authority of Singapore; Deloitte; Bank of America Merrill Lynch; BCS Information Systems; Credit Suisse; DBS Bank; HSBC; J.P Morgan; Mitsubishi UFJ Financial Group; OCBC Bank; R3; Singapore Exchange; UOB Bank. 2017. Project Ubin; SGD on Distributed Ledger.

Monetary Authority of Singapore; The Association of Banks in Singapore; Monetary Authority of Singapore. 2017. Project Ubin Phase 2.

Monetary Authority of Singapore; SGX; Anquan Capital; Deloitte; Nasdaq. 2018. Project Ubin: Delivery versus Payment on DLT. South African Reserve Bank. 2018. Project Khokha: Exploring the use of DLT for interbank payments settlement in South Africa.

Sveriges Riksbank (Swedish Central Bank). 2017. The Riksbank’s ekrona project report 1.

Sveriges Riksbank (Swedish Central Bank). 2018. The Riksbank’s ekrona project report 2.

Sveriges Riksbank (Swedish Central Bank). 2018. Economic commentaries: Are Bitcoin and other crypto-assets money? And more.

Introduction to Central Bank Digital Currencies (1/2) was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.