Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

As Shrimpy continues to grow and expand its product features for the crypto world, one of our most frequently asked question is — What is the optimal rebalancing strategy for me? Given the variety of trading fees imposed by the various exchanges and trading platforms, the portfolio performance of automated rebalancing strategies may differ when deciding which exchange or trading platform to primarily conduct trades on.

This study will take a closer look at the effect of trading fees and their effect on portfolio performance.

Analysis

SOURCE

The data for this study was provided by CoinAPI. Using their rest APIs, we were able to compile the 20 best bid prices and 20 best ask prices available on Bittrex at each rebalance time interval. Our data begins on March 15th 2017 and continues until October 20th 2018.

CoinAPI is a service which collects data from countless exchanges. Applications such as Shrimpy can then use that data to construct accurate backtests, market analysis, and produce comprehensive research.

TRADES

- Fee — All trades included the relevant fee (0.0001%, 0.05%, 0.10%, 0.15%, 0.20%, 0.25%)

REBALANCE PERIOD

- Rebalance periods — 1 hour, 1 day, 1 week, and 1 month

Learn more about rebalancing for cryptocurrency.

PORTFOLIO SIZE

- Initial portfolio value — $5,000

- Number of assets — 10 assets per portfolio

Learn more about how the number of assets in a portfolio affects performance.

ASSET SELECTION

- Portfolio construction — Randomly selected from assets available between 3–15–17 and 10–20–18 on Bittrex

Learn more about how to build a strong portfolio.

BACKTEST

- Number of backtests — 1,000 backtests per trading fee & rebalance period pair

Read more about backtests or run your own.

RESULTS

The performance for each backtest was determined by taking the final rebalancing value and comparing it to the final buy-and-hold value. This was done by using the equation: (Rf — Hf) / Hf, where Rf is the final rebalancing value and Hf is the final buy-and-hold value.

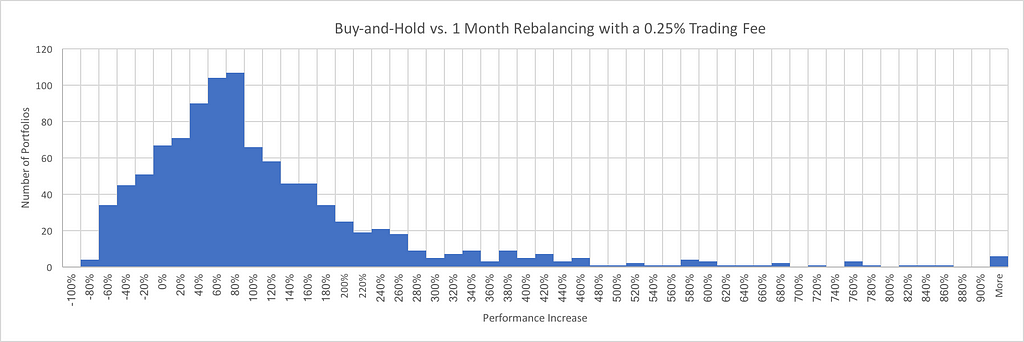

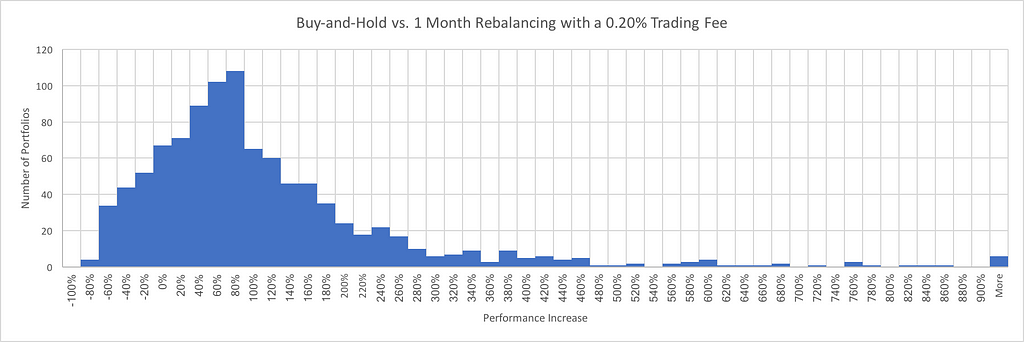

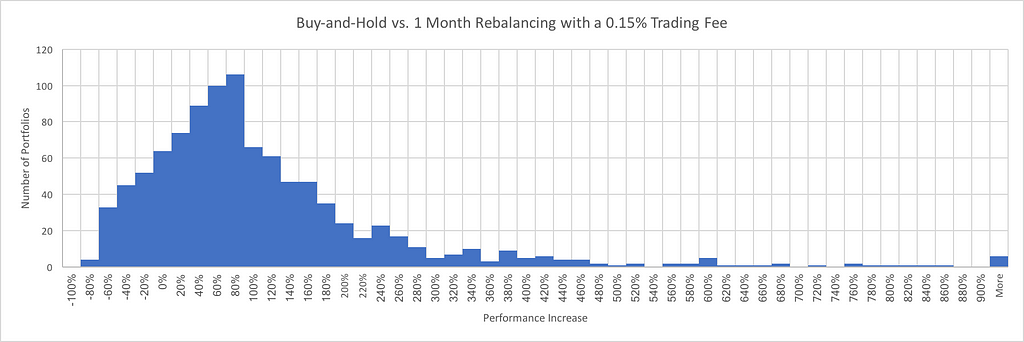

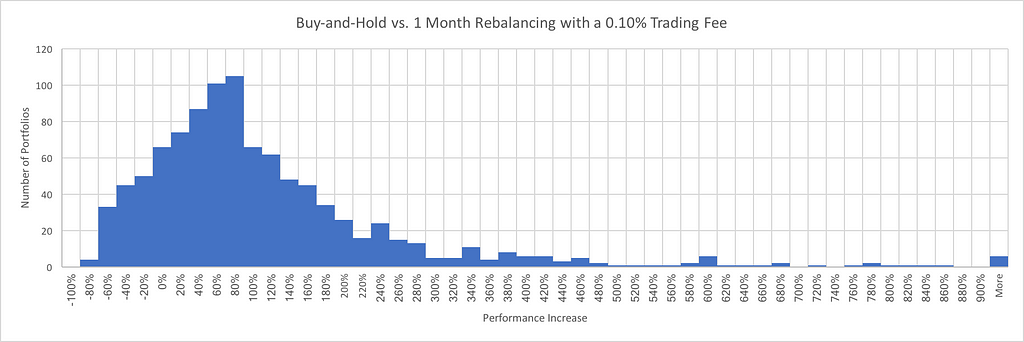

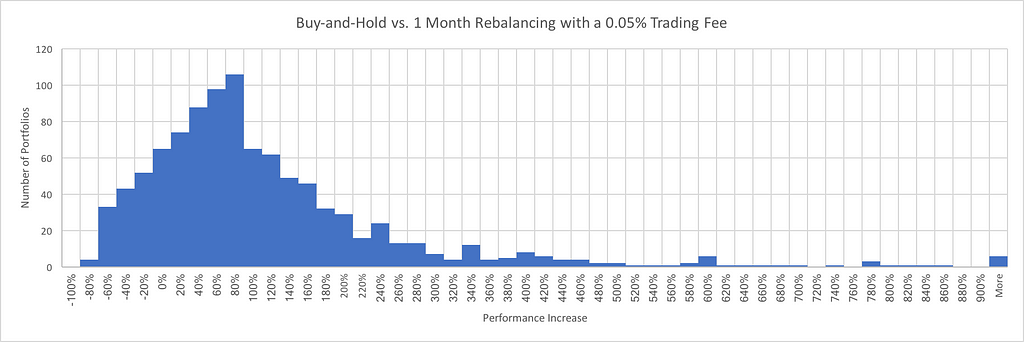

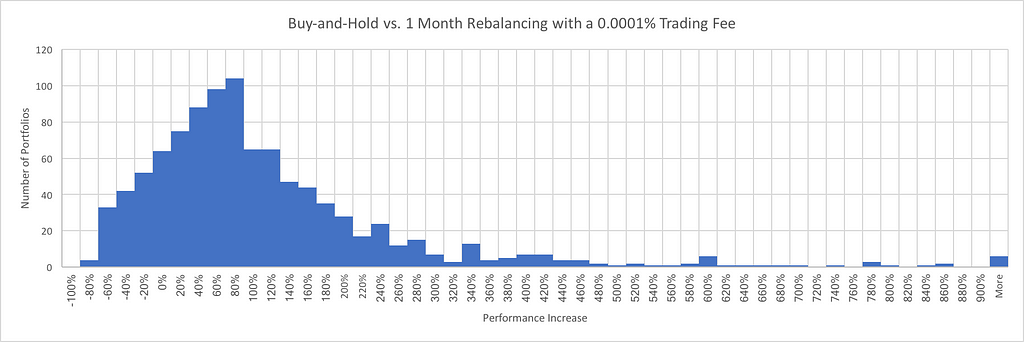

1 Month Rebalance

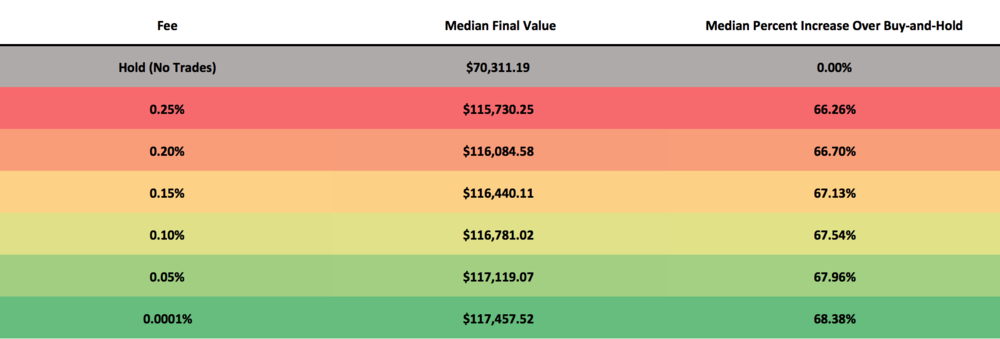

A 1 month rebalance period experienced the least performance drift, among all rebalance periods examined, as the fee increased. Thinking about the comparison between different rebalance periods conceptually, it’s reasonable to reach an expectation that monthly rebalances should be affected less from fees since monthly rebalances perform significantly fewer trades than shorter rebalance periods. As assets drift in price, they frequently oscillate or change direction, so the price of an asset is rarely always increasing or always decreasing. All of the oscillations that take place throughout the month period won’t be captured by a monthly rebalance. However, these direction changes will be observed by more frequent rebalances, resulting in higher trade volume and fees. Additionally as a result, monthly rebalances experienced the least benefit from decreased trading fee of any rebalance period studied.

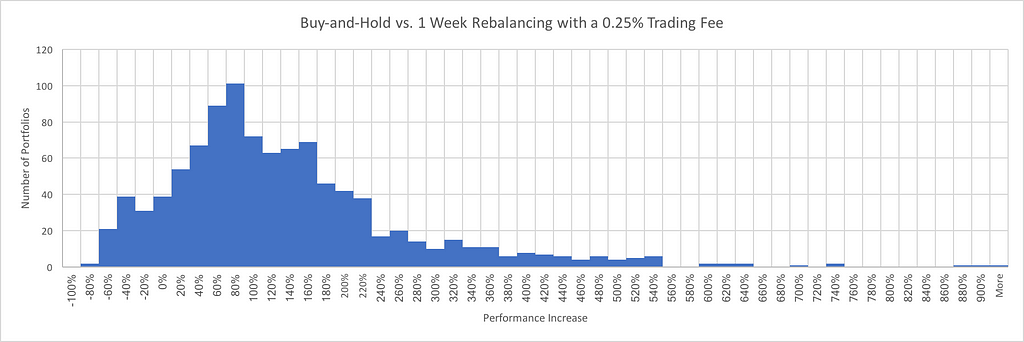

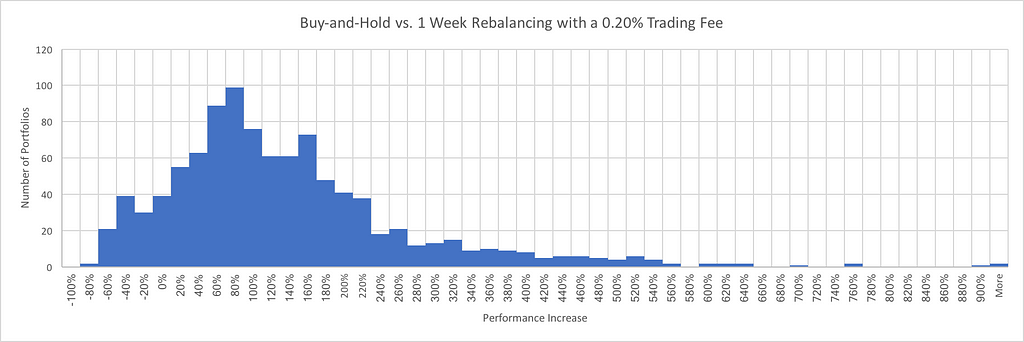

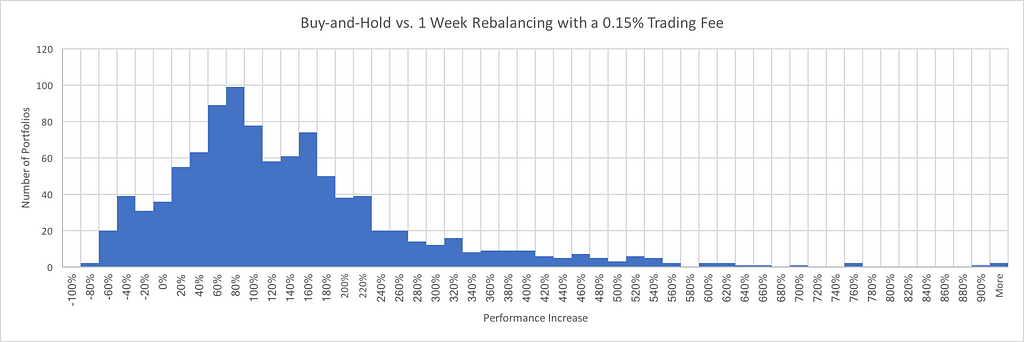

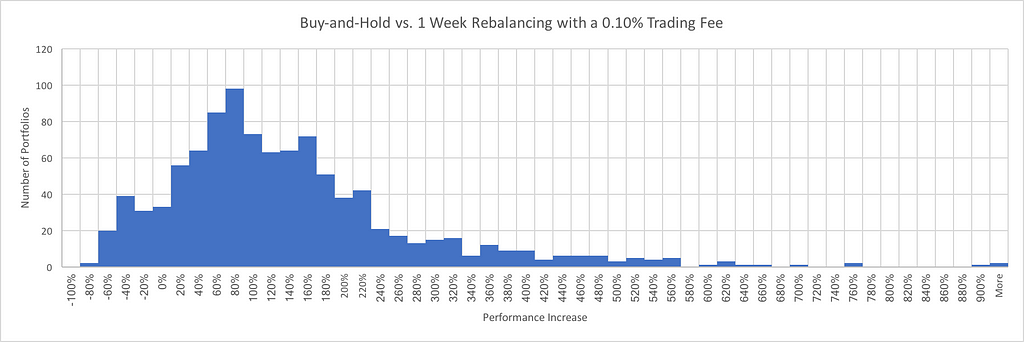

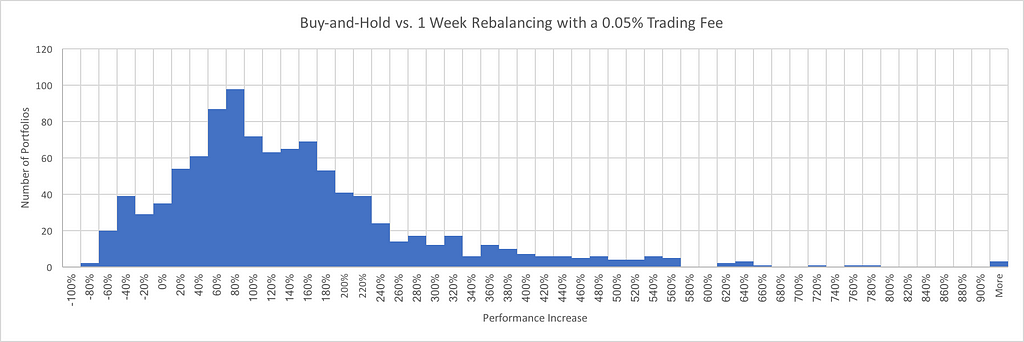

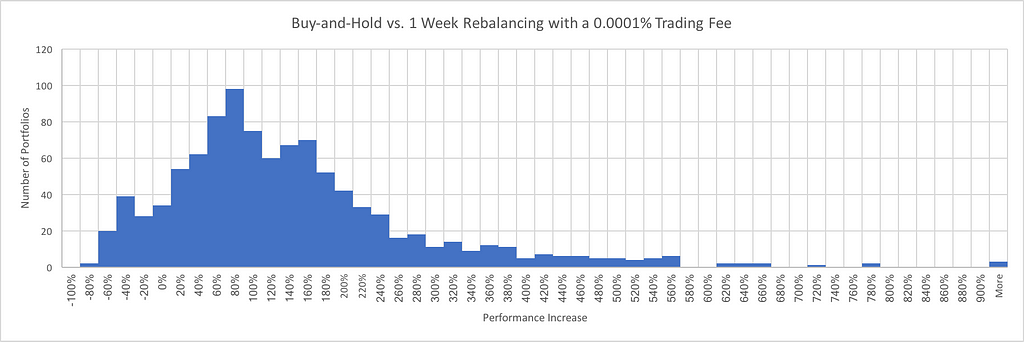

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,311.19 which was achieved for buy-and-hold suggests a median performance increase of 1,306%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Week Rebalance

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,311.19 which was achieved for buy-and-hold suggests a median performance increase of 1,306%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Week Rebalance

A 1 week rebalance period demonstrated a performance increase of ~ 30% when compared to monthly rebalancing. Similar to how monthly rebalancing didn’t result in a large performance boost when decreasing fee, weekly rebalances only observed a ~ 5–6% increase in performance. While every percent matters, the next backtests which look at daily and hourly rebalances will demonstrate a more profound change in performance.

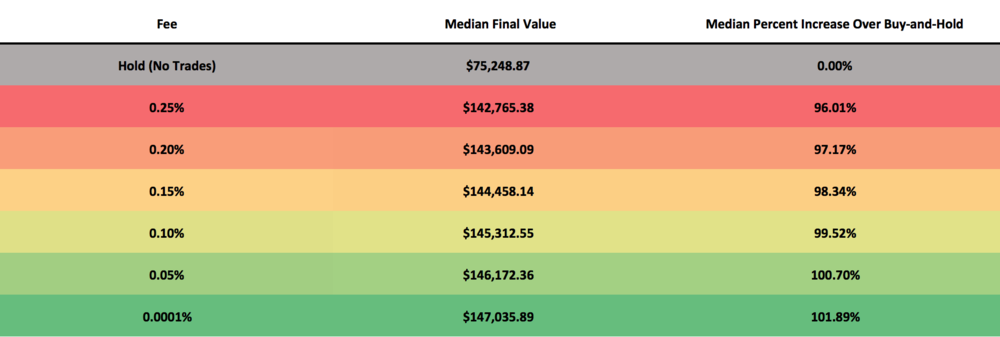

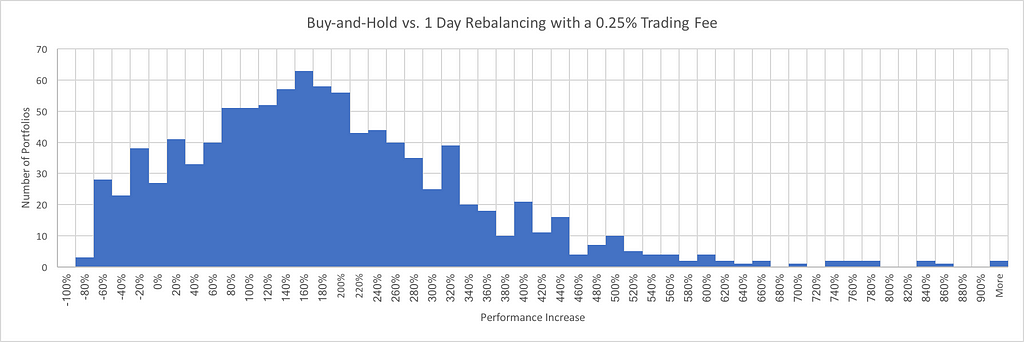

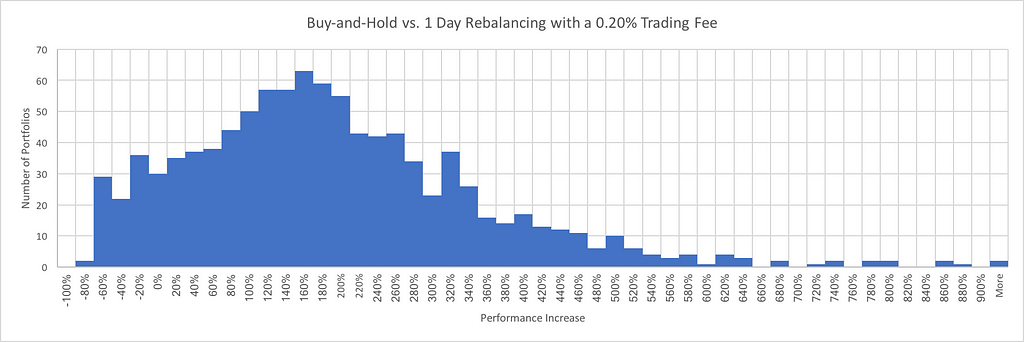

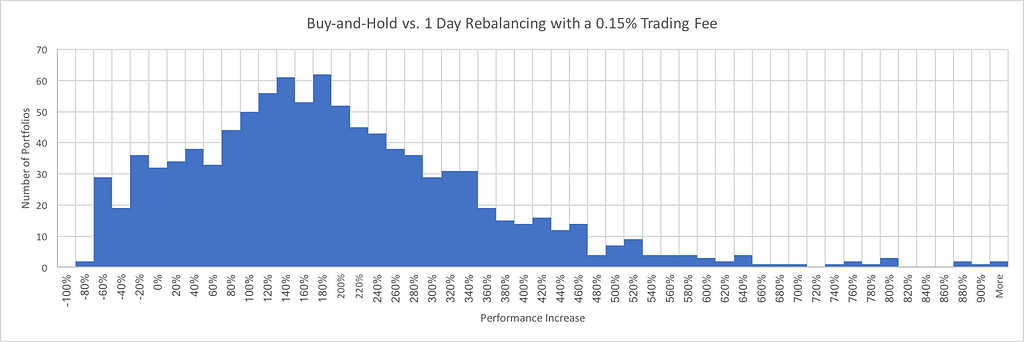

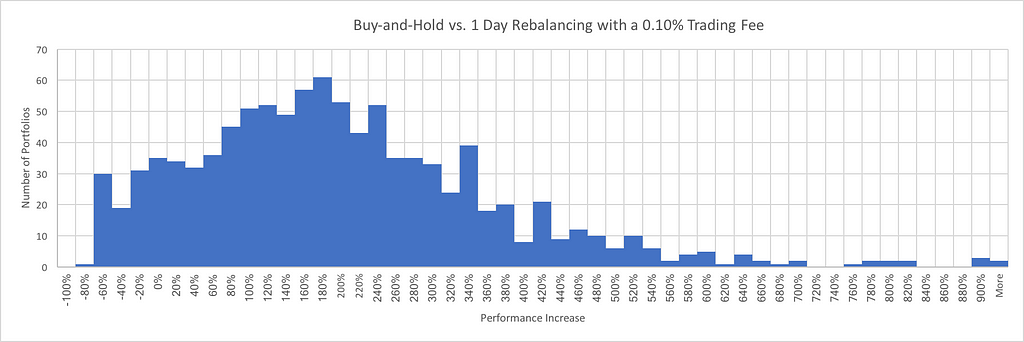

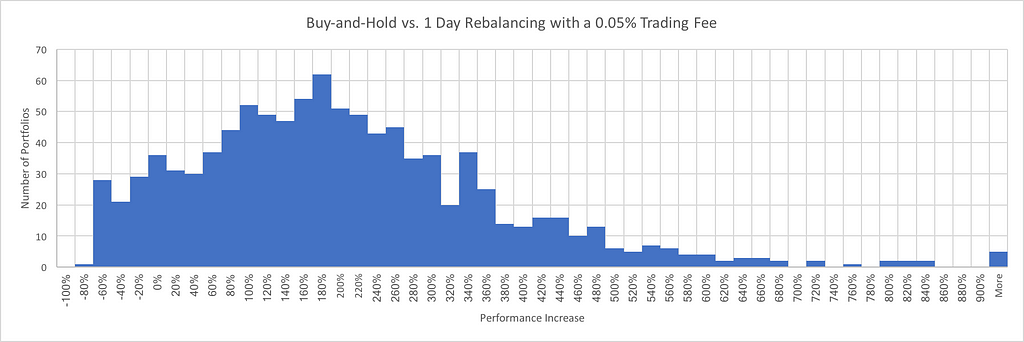

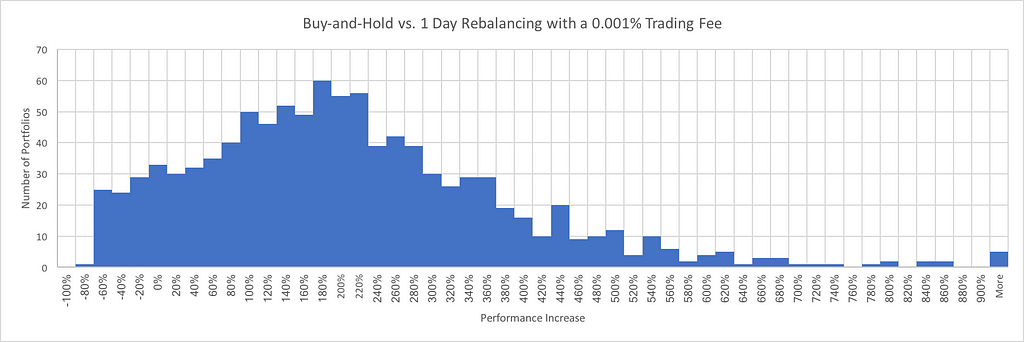

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $75,248.87 which was achieved for buy-and-hold suggests a median performance increase of 1,405%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Day Rebalance

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $75,248.87 which was achieved for buy-and-hold suggests a median performance increase of 1,405%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Day Rebalance

Daily rebalances emerged as the highest performing rebalance period when taking into account all trading fees that were examined. The only fee which demonstrated a clear improvement over daily rebalances was the 0.0001% trading fee. When compared to monthly rebalances, daily rebalances had a difference of over 60% for all trading fees studied. In addition, we can see a 20% performance difference between the 0.25% trading fee and the 0.0001% fee. Such a large range of performance results illustrates the importance of reducing fees for portfolios that utilize a daily rebalancing strategy.

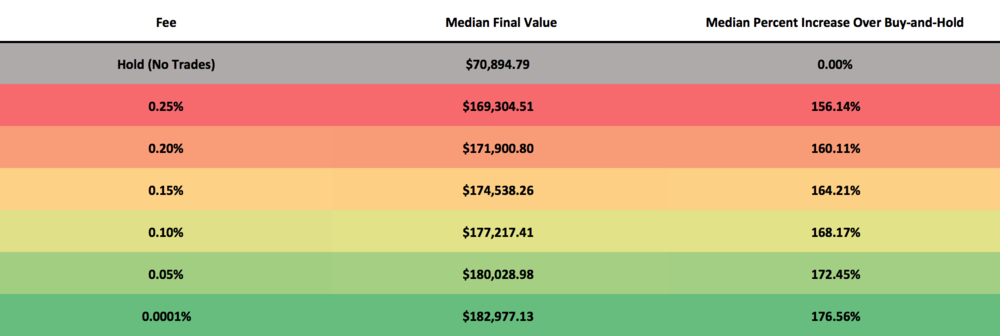

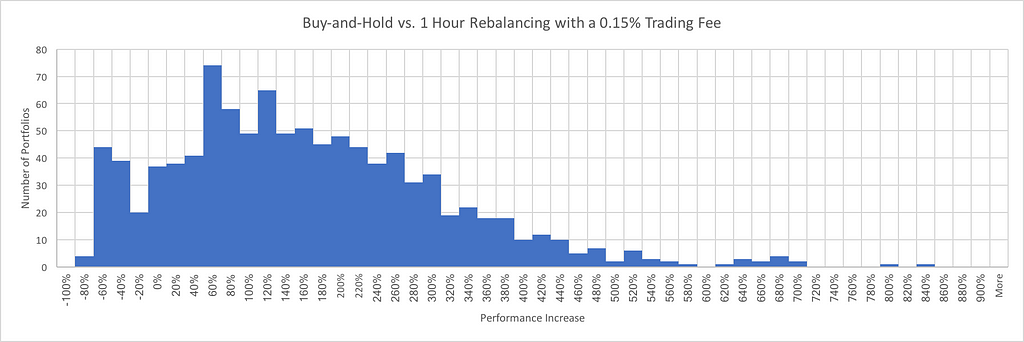

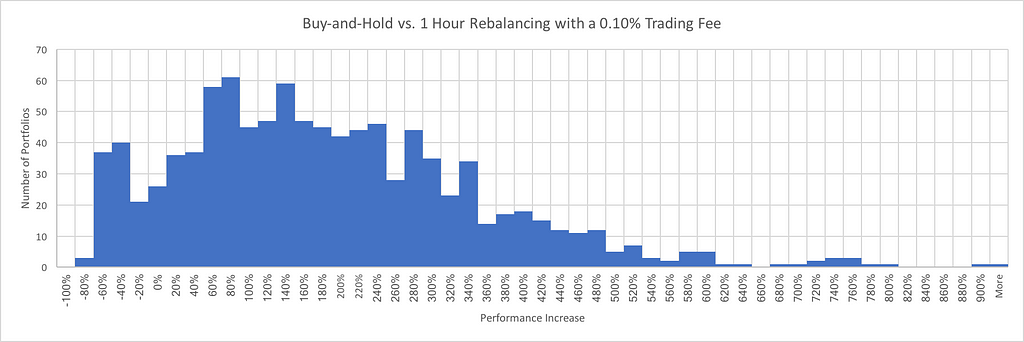

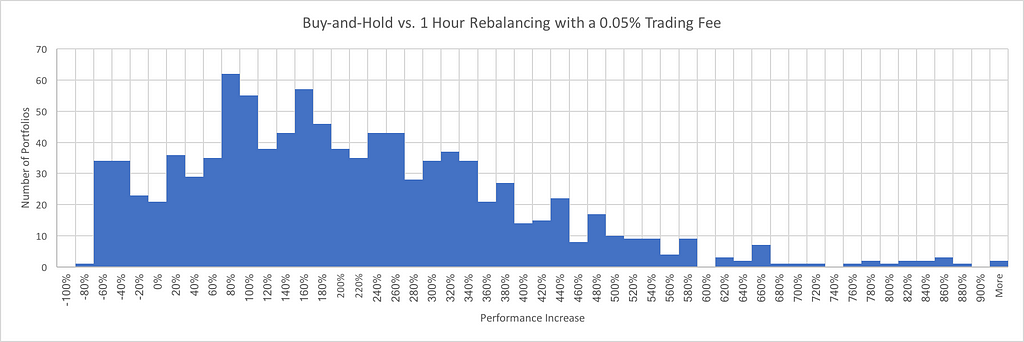

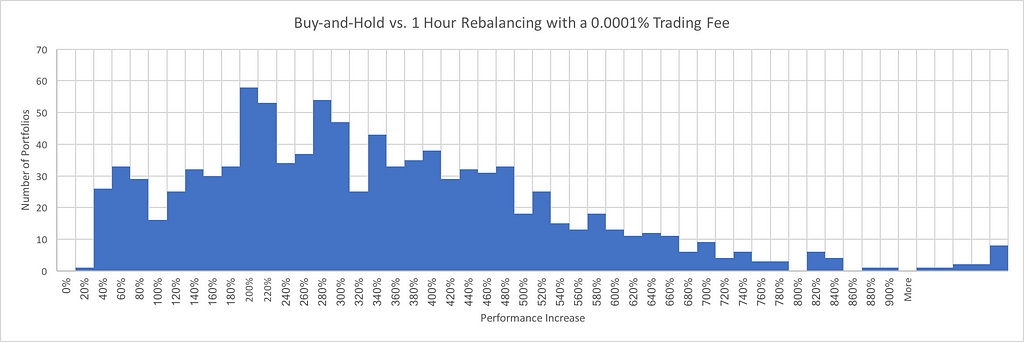

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,894.79 which was achieved for buy-and-hold suggests a median performance increase of 1,318%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Hour Rebalance

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,894.79 which was achieved for buy-and-hold suggests a median performance increase of 1,318%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.1 Hour Rebalance

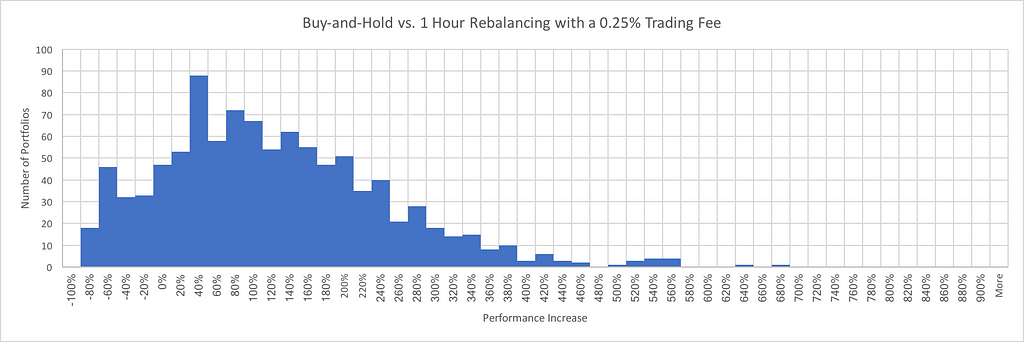

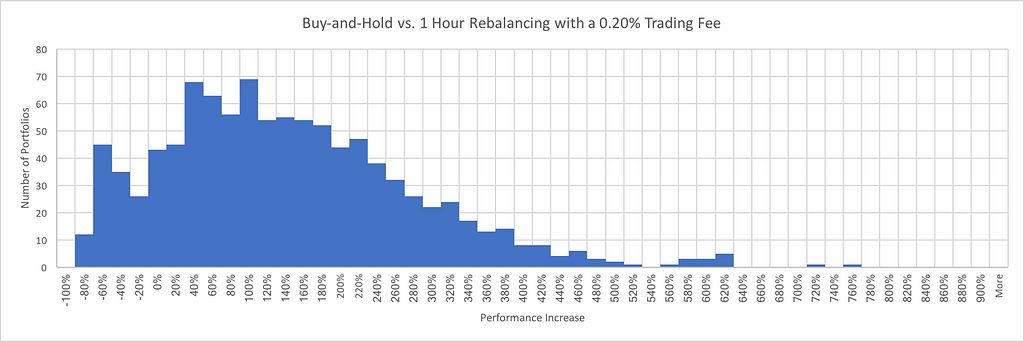

Hourly rebalances produced the widest range of performance results. Starting with a 94.28% performance boost when using a 0.25% trading fee, hourly rebalancing achieved lower outcomes than both daily rebalances and weekly rebalances. However, as the trading fee reduced, hourly rebalances increased in performance rapidly. This rise continued until hourly rebalances outperformed all other examined rebalance periods as the trading fee approached 0.

The results highlight the attention that should be placed into lowering trading fees if a hourly rebalance period is being executed. With a ~ 100% performance difference between the highest and lowest fee tested, the trading fee has a critical importance to the success of this portfolio strategy.

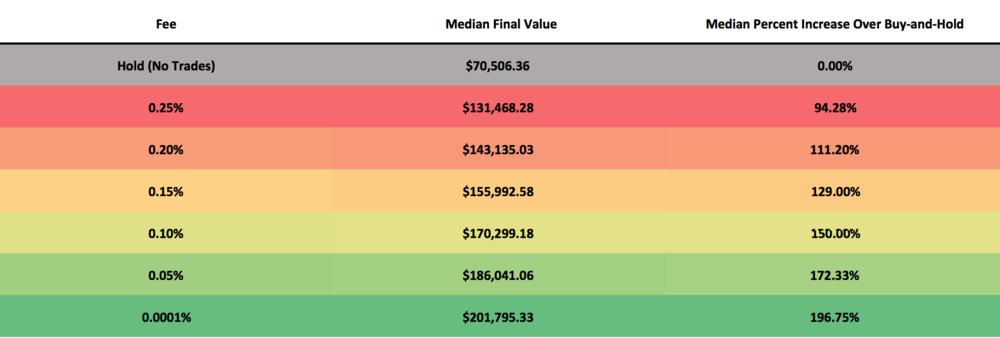

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,506.36 which was achieved for buy-and-hold suggests a median performance increase of 1,310%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.

This table illustrates the median performance of 1,000 backtests which were run with each of the trading fees depicted above. The median final value is the value of the median portfolio after the backtest is complete. Each backtest is allocated $5,000 at the start, so a final value of $70,506.36 which was achieved for buy-and-hold suggests a median performance increase of 1,310%. The median percent increase over buy-and-hold is how much better the median final value performed than the median buy-and-hold value.

CONCLUSIONS

Comparing all the results in a single graph, we can get an interesting picture of how trading fees affect the performance of each rebalance frequency. From the graph, we can see that when we approach a scenario with no trading fees, the optimal strategy is hourly rebalancing.

From these results, we can conclude that trading fees can have a large impact on portfolio bottom line performance. In the perfect world with no trading fees, hourly rebalancing proves to be the optimal strategy,

However, we also observe that in a real-life scenario with trading fees, a daily rebalancing strategy shows the most consistent portfolio returns. Even for hourly rebalancing, the trading fees will have to be as low as .05% to match the return from a daily rebalancing strategy.

From this analysis, we can conclude that trading fees may have a large impact on the performance of various rebalancing strategies. The immature and volatile nature of the crypto space presents unique opportunities for managing and executing a rebalancing portfolio strategy.

Disclaimer: Backtests examine past performance and do not guarantee future performance.

REBALANCING WITH SHRIMPY

Shrimpy is a free application which automates the rebalancing strategy. Our dedicated tools for asset allocation, backtesting, and indexing the market are the most powerful in the industry. Whether you are an institution or individual, our solutions are designed to solve the most pressing problems facing portfolio management in the crypto space.

Sign up today by clicking here.

If you still aren’t sure, try out the demo to see everything we have to offer!

Don’t forget to check out the Shrimpy website, follow us on Twitter and Facebook for updates, and ask any questions to our amazing, active communities on Telegram & Discord.

Leave a comment to let us know your experiences with rebalancing!

The Shrimpy Team

Originally published at blog.shrimpy.io.

Crypto Portfolio Rebalancing: A Trading Fee Analysis was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.