Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

Why & How to tokenise a Venture Capital Fund?

Photo by Marta Branco from Pexels

Photo by Marta Branco from Pexels

Part I : Traditional VC landscape

A note about how VC firms raise & invest capital

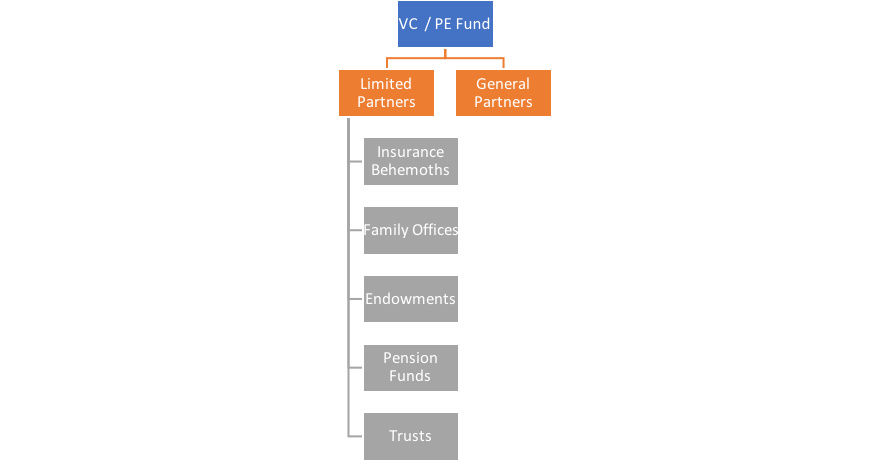

Entities involved in a VC fund

Entities involved in a VC fund

Traditional Venture Capital (VC) funding is an interesting landscape. There are early stage funds, Late stage funds, Specific technology focussed funds, Fund of Funds, Funds which are Super Giant sized, Funds which are vintage (#oldmoney), Funds that are fairly nascent. KPMG published an interesting global analysis of Venture Funding

It is a competitive environment for VC fund managers to raise funds in the first place

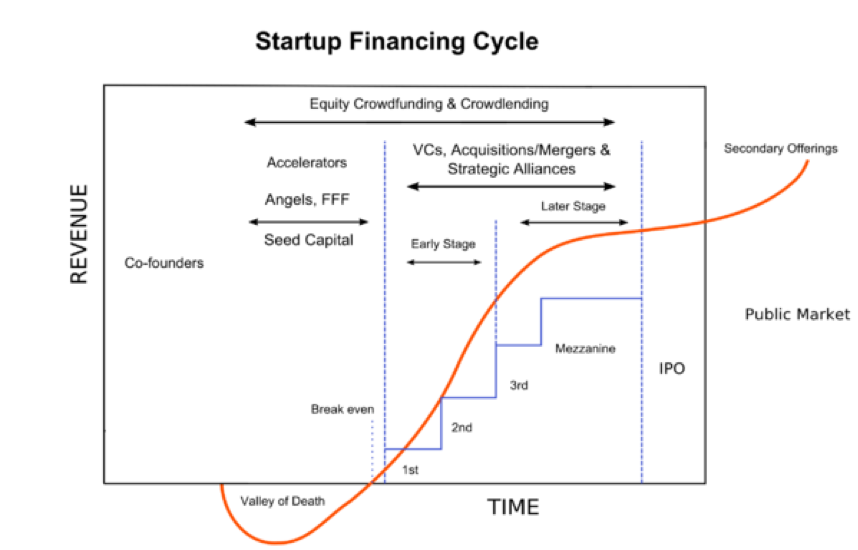

Source: File: Startup Financing Cycle.png — https://en.wikipedia.org

Limited Partners provide Capital Contribution while General Partners invest the fund pool into multiple companies on the basis of a defined investment strategy.

These invested companies are collectively termed as that VC fund’s portfolio

Invested companies are expected to perform well over time (usually 5–7 years) and provide an appreciation on the invested capital by way of up rounds. The appreciated returns, after realisation by way of exits, are passed back to Limited Partners as the Fund’s Income Distribution

The job of Sourcing, Investment Analysis, Due Diligence, Portfolio management is challenging and involves a mixture of soft skills, patience, network effects in the industry and financial juggling. General Partners are paid for these challenges by Limited Partners as Annual Management Fee (typically about 2% of funds under management)

If a return of investment is realised in a Liquidity event (successful exit from a company), then a profit distribution of aprox 20% net of promised fund performance (carry) is paid to the General partners.

If a Tech startup company founder is looking for funding, It is not dissimilar to the situation of a VC looking to raise funds for their vehicle. The similarities ends there as founders of tech companies have only one chance to succeed / fail in that company. A fund manager (VC) on the other hand deploys the fund across multiple companies taking calculated risks. This has a distributing effect of high risk & playing to the fact that mathematically, the probability of at least one of the portfolio companies performs in a stellar fashion, it may pay off to average out the other failures

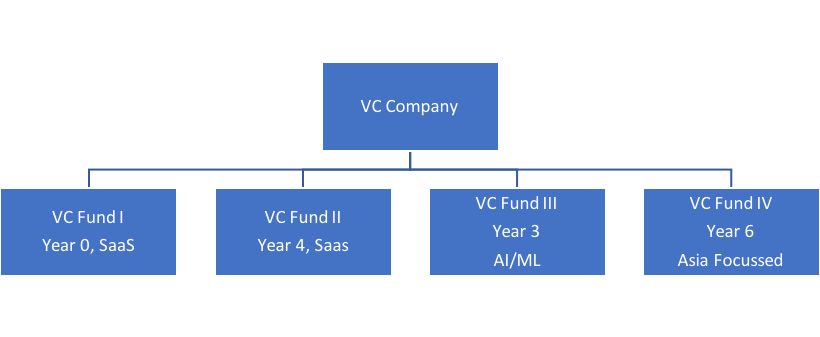

A VC firm may have multiple funds with different goals. This is an Example.

A VC firm may have multiple funds with different goals. This is an Example.

Challenges faced by GPs & LP’s (this list will be discussed in detail in an upcoming blog post)

1. Unreasonably long Time horizons to realise Returns. The time horizon for a company to return some appreciation, if at all, is about 5–7 years. This leads to the next challenge

2. Low Liquidity for LPs. Limited partners are briefed by the GP’s at the time of a fund raising effort that their investments are unlikely to yield any returns prior to year 7. A clause sometimes restricts LPs from trading/selling their investments to other parties. Therefore, a LP may have to wait it out up to year 5 to even see a hope of an exit

3. Very high uncertainty / Challenging ROI: Most start-ups fail! Many studies say upwards of 95% of all start-ups fail. When a start-up fails after investment, it is a zero ROI on the money & negative ROI on the time invested

4. Information Asymmetry: exists in LP-GP relationships as well as VC-portfolio company relationships

5. Portfolio effect to mitigate the high risk: Both LPs and VCs build a portfolio to spread the risk. But in both cases, the portfolios are more or less illiquid

6. Raising another Fund: How will LP’s trust the GP if they haven’t yet returned any cash let alone profits? It is a serious problem for the majority of the VC firms.

According to a deep dive by Crunchbase,

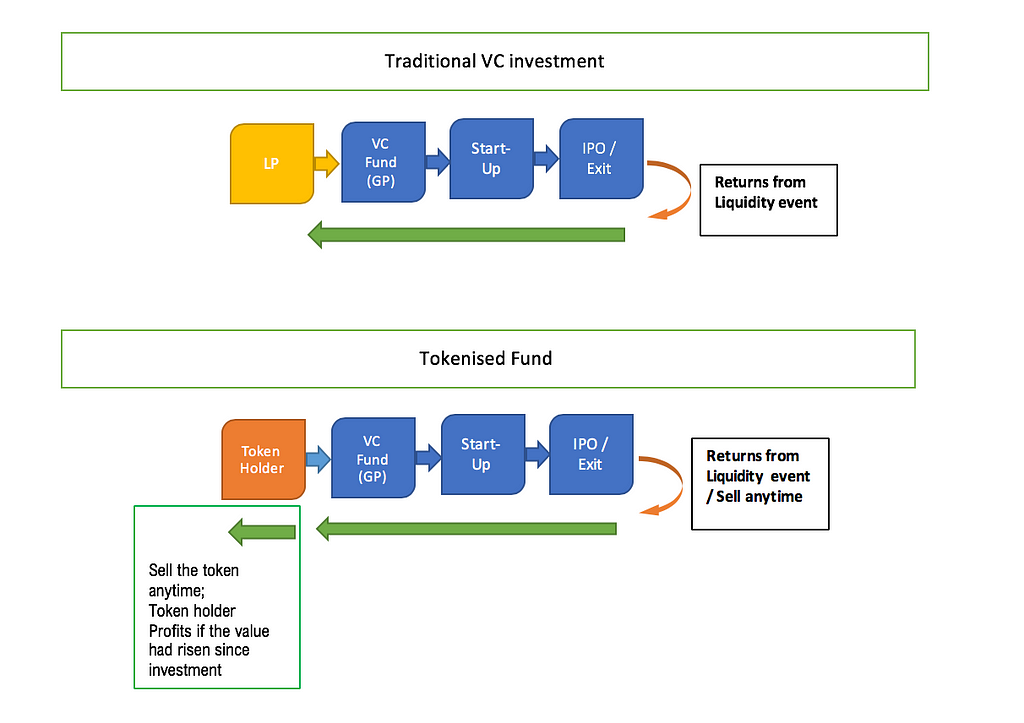

When it comes to investing in private companies, putting money into a venture is often the easy part. It’s getting the money out — and hopefully more than at the start — that is the stickiest wicket in the whole process.An “exit” by way of merger or acquisition is among the most common ways startup investors are able to liquidate their long-held stock positions. The Liquidity comes from being able to sell the tokens

The Liquidity comes from being able to sell the tokens

Part II: Tokens & Tokenised funds : What are they & how are they beneficial

Tokens are programmable. Underlying assets can be linked to tokens using Blockchain. They are lines of code that can execute automatically to deliver outcomes based on logical triggers that are pre-programmed at the time of coding.

The business logic can be pre-programmed into the code itself. Therefore, the tokens can be programmed to:

1. Stay put in a wallet for a certain amount of time (Minimum commitment time)

2. Only be sold in the secondary market to entities who had undergone fixed KYC procedures (can be programmed to follow KYC/AML/CTF laws)

3. Only be sold to people who are Accredited investors (in certain jurisdictions)

4. Include the governance of the LP-GP management terms agreed at closing of the fund

A tokenised fund can be viewed as equity crowdfunding of a VC fund.

The token sale raises capital in exchange for either equity of the VC fund or promise of income distribution from the token fund vehicle. These tokens are termed as Equity tokens or Security Tokens. The fund raising token sale is termed as a Security token offering.

The governance and application of legal oversight still remains the same if the token sale is conducted in the same jurisdiction that the fund normally operates from.

The fund will still need to comply with any reporting, auditing, notification and filing formalities that are normally associated with the operation of funds in that jurisdiction.

The token sale plays the role of replacing a handful of institutional investors with a larger number of institutional investors / accredited investors.

NB: Tokenised funds may in some cases invest in tokenised firms seeking investments. The liquidity of those investments in such cases is much higher as their portfolio is itself tokenised & tradable.

How tokens can solve the challenges / provide new benefits

(a) Providing liquidity for LPs:

Since the LP’s are at the most limited from trading/selling their tokens for 12months, in a tokenised fund, they gain radically more freedom in liquidating their positions in the secondary market. This benefits the LPs in deploying capital elsewhere as they see fit. The freedom that is gained will increase the likelihood of LPs investing in funds they would not have otherwise. This would lead to a cascading effect of entrepreneurs receiving funds for their ideas quickly as VC’s themselves can raise funds far more easily.

(b) Solving alignment issues:

Extensions at the end of a Fund are common misalignment between LPs and GPs. A GP may be minded to wait it out for a portfolio company to take its time to perform well & may request an extension beyond the agreed 10year fund life. Typically, extensions are for a 1 or 2 year period to allow for the portfolio position to be wound down. They are usually pre-written in the fund agreement

However, an LP may have to agree to such an extension even if their preference is not to.

Faced with a similar situation in a tokenised fund, LPs have an option to sell their tokens / positions in the secondaries market

( c) Tokens are Globally tradable

By design, tokens are easily tradable worldwide on crypto exchanges. Yes, a secondary market for LP positions exists in the traditional world. However, it is very illiquid and can be a very slow process. By design in a tokenised fund, an LP may exit and re-enter a fund multiple number of time if it suits them. In a traditional VC landscape, LPs who liquidate their positions can only do so in the fund’s native jurisdiction. Such restrictions do not apply to tokens as they can be traded globally.

(d) LPs are getting more risk savvy. Tokens are a way of quick feedback

Tokens provide a convenient avenue for LPs that have an enhanced risk appetite to invest directly in early stage start-ups.

(e) Shorten Feedback Loops & increase IRRs for GPs

Liquidity in a tokenised environment may provide GPs in a VC firm a shorter feedback loop. Those GPs who realise a better IRR in a shorter feedback loop will be better positioned to raise a new fund. This removes the problem of not being able to raise a new fund in traditional VC landscape with long feedback loops.

(f) Sidestep the issue of Preferred return hurdle (PRH)

This is a contentious issue in the LP-GP relationship. Most GPs 20% carry does not consider the time value of money — the GP’s carry is solely based on the cash-on-cash return of the fund. A preferred return hurdle (PRH) changes that dynamic in the LPs favour.

A PRH of 6% simply means that the LP’s must preferentially receive a 6% annual appreciation on the capital invested first before GPs earn any carry. This is an issue that is created in the traditional illiquid setup.

However, in the tokenised environment, fewer LPs will remain invested long enough for the time value of money to be significant. This is a side stepping of a sticky subject in a tokenised environment

Note: Yes, a VC fund can be IPO’d but it is highly expensive and a friction filled process

Closing remarks:

Tokenising provides opportunities to let go of the rigid positions of GP’s & LPs in traditional finance. It allows LPs and GPs to map investment efforts collaboratively. The change in dynamic between GPs and LPs also cascades down to the start-up ecosystem. Easier access to capital will result in far more entrepreneurs chasing their dream.

Written by: Suraz Kottakki & Dr. Joel Palathinkal

Finally, a word about Genesis Block Holdings:

Genesis Block Holdings is a blockchain venture capital firm, crypto quant hedge fund, and mining company focused on investing in blockchain projects within the ecosystem. We are laser focused on bringing the power of capital, network, and expertise to frontier technology teams to solve the world’s biggest problems

Under no circumstances should any material on this post be considered as an offer to sell or a solicitation of any offer to buy an interest, token or coin in any individual company or investment fund. Any such offer or solicitation will be separately made only by means of the Confidential Private Offering Memorandum relating to the particular fund or persons who, among other requirements, meet certain qualifications under U.S. federal or other international securities laws and generally are sophisticated in financial matters, such that they are capable of evaluating the merits and risks of prospective investments

If you felt this was helpful, please clap for us, share it amongst your friends and feel free to send us a note anytime at genbvc.com. Checkout our telegram channel here> and follow our blog here>

{kind=link}

Why & How to tokenize a Venture Capital Fund? was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.