Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

- The biggest US banks predicted the price of Brent crude oil in 2024 at $90-94

- Actually, the price fell to $70 a barrel in the third quarter, making many US oil projects unprofitable, forcing companies to cut drilling rigs

- JPMorgan underestimated demand by 600,000 barrels per day in the third quarter of 2024

- BRICS countries, including China, import oil from Iran bypassing Western supplies and banking systems

- BRICS and OPEC are creating a new blockchain-based trading system, that could change global energy markets

Forecasts about oil prices and demand for 2024 from US leading investment banks, such as Barclays, JPMorgan, and Goldman Sachs became highly inaccurate, and the return on investment in US oilfield development is not justifying itself more and more.

Among other factors, the BRICS countries are playing their part in many ways, and the growing oil trade between China and Iran is the most telling example.

All of this probably has far-reaching plans, and there are signs of an actively developing alternative economic union and blockchain-based financial system.

What’s at the Table Today on Oil Prices and Demand

Late last year in 2023, US investment banks and energy agencies presented their forecasts for oil demand and price in 2024.

Barclays is the London-based bank that finances most of Europe’s energy trade and it predicted that the average price of Brent crude will be $93 a barrel in 2024.

Most of the other forecasts coincided with them, the US Energy Information Administration (EIA) predicted the price will also be $93, Bank of America predicted an average price of $90 per barrel and Goldman Sachs predicted $94 per barrel.

The third quarter of 2024 is coming to an end and we do not see a price of $90-94, and even more the price has fallen from $90 in April to $70 now.

This miscalculation by the investment banks who predicted that the average price of $93-94 per barrel in 2024 is much more important than it may seem. It is fundamental information that their clients in the energy sector have drawn up CAPEX capital expenditure and production schedules for the energy companies’ fields and made the corresponding CAPEX investments.

But how could such large investment banks have miscalculated so much, and what do blockchain and cryptocurrencies have to do with it? Likely, play a key role, they largely allowed this to happen, and, even bigger news is just waiting for us.

Oil Producers are Facing Now Two Issues

The first, to be fair, is the actual drop in demand associated with the electrification of transportation in China and the available Chinese clean energy technologies.

China is actively carving out a niche with its alternative solutions, exporting this to developing countries. They should have become a huge new market for oil companies during their development, but due to the electrification of transportation and Chinese clean energy technologies have not.

The second aspect is less obvious, even though we hear open information about it all the time, and that is the BRICS countries, which are also changing their preferences for energy suppliers.

It’s important to note that alternative clean energy solutions have not displaced oil, oil demand is still high, but it’s shifting away from US suppliers and US banks are no longer seeing these BRICS markets.

JP Morgan specifically for Rison explained that they also got their forecasts wrong, global oil demand was 600,000 barrels per day less than they had forecast for the third quarter of this year, and also overestimated the average oil price of $94 per barrel.

For consumers, the fact that oil prices are much lower is generally good news, and it could also have some impact on inflation and the fact that the FED has cut rates.

However, the opposite is true for producers, as most major oil fields in the US become profitable at $90 a barrel and start losing money at $70.

Look, this is a break-even chart of oil prices across the US, where the blue line shows where the price of WTI oil must be for the wells in these fields to be profitable.

WTI is the West Texas Intermediate oil price which is the benchmark for oil prices in the US and yesterday their index closed at $67 and in the Permian Basin oil producers need at least the full $70 before they can start to profit from new wells in all US fields.

These breakeven levels are too high to justify new CAPEX investments in oil fields so this producer’s place is simply scaling back its plans. We see that US energy companies are reducing the number of active drilling rigs in the US this reduction has been seen in five of the last six weeks, after having already reduced the number by 20% last year.

So, new capital investment is falling and will probably continue to fall, the rig count is declining and companies will lay off employees, all because last year US banks and energy companies got their $90 forecasts inaccurate.

Forecast Inaccuracy Reasons, and BRICS Impact

But how could they be so inaccurate, especially as prices continue to fall? Actually, they weren’t entirely wrong about the oil demand, and with that demand, the oil price really should be. However, they were wrong about who would meet that demand, which we touched on a bit earlier.

It turns out that the BRICS and OPEC countries, without official statements, though not without many hints and showcasing initiatives, are creating an alternative economy space, you guessed it, with a blockchain-based financial system, which has never happened before since the creation of the petrodollar.

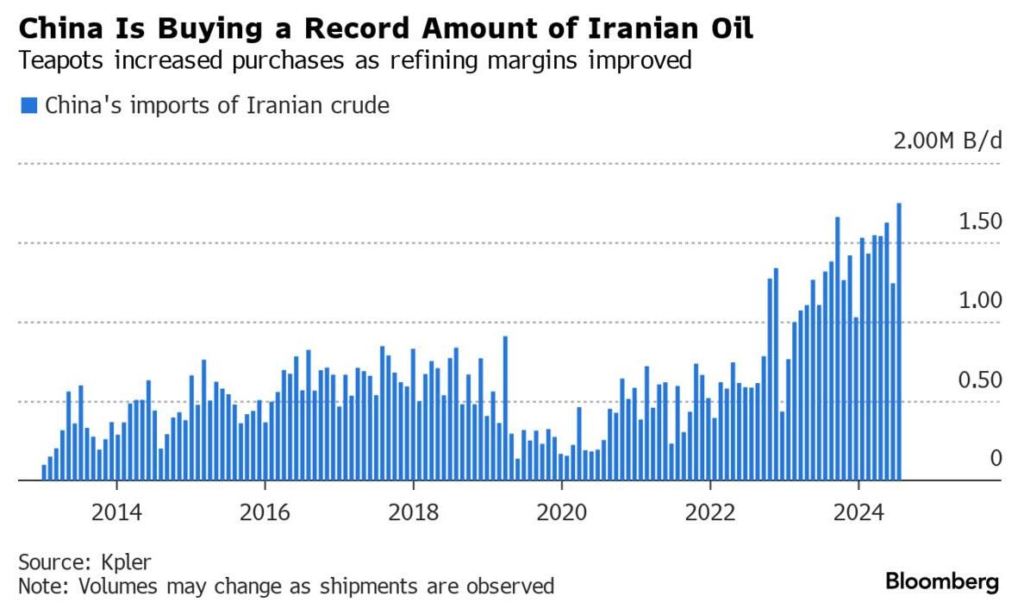

Now with this new trading system, they are bypassing Western banks and Western energy companies and Western trading systems are shrinking. They no longer need American oil suppliers and of course, they don’t need American banks, for example, China is importing record amounts of crude oil from Iran.

Look at this chart which indicates that last month in August China imported 1.75 million barrels per day, a 50% increase over the previous month and an all-time record.

This is also confirmed by an interview with an expert on NPR, with an explanation of the reasons for this miscalculation by JP Morgan. They say that China’s demand for oil was lower than expected. However, as you can see, this is only part of the truth, as demand from China has not dropped, it’s just that they are doing business with Iran and other BRICS countries instead of US suppliers.

Barron tries to understand the implications of this and compares forecasts from British Petroleum and OPEC.

BP, one of the world’s largest oil companies, says that global oil demand will peak next year, then level off, and then fall forever after that. OPEC, on the other hand, believes otherwise, that oil demand is growing and there will be no end to it, or to be a bit more precise, that oil demand will grow for another 20 years.

Barron wonders how such serious players can differ so much in their estimates, but as you have probably figured out by now, there is no contradiction. For transnational oil and gas BP demand will fall, for OPEC demand will rise because they are taking sales away from BP and other western oil giants.

This means that suddenly global markets are slipping out of the hands of Western energy producers, and what’s more, if this trading system moves to a private blockchain, they won’t even know the volume of trade, who is actually buying what, who is buying from whom, how much is being bought and sold.

Even the current market estimates, before the transition to a private blockchain and while trading is done mostly in Yuan – the numbers don’t add up anymore. OPEC states that oil demand in the first quarter was 103.5 million barrels per day, while EIA states 101.7, which is a very large difference in numbers and a field of maximum uncertainty for investors.

Probable BRICS Vector and Blockchain as a Key Technology

We will probably have to get used to it that an increasing portion of the world’s oil trade will be conducted outside the U.S. and European banking systems. In turn, U.S. industry executives and investment banks will now be unable to understand even basic information like the size of demand, how and by whom that demand is met, and what prices are paid.

Economic sanctions against Venezuela, Iran, and others have only prompted oil producers to find ways around them. China and Iran found a way around Western banks and transportation systems, now other sanctioned countries or those countries afraid of being sanctioned are joining the process.

In turn, the urgent adoption of Bitcoin by the U.S. and the importance of this to maintaining its economic leadership is making more and more sense. Probably, the BRICS countries are not working on an alternative trading and financial blockchain-based system to move everything to Bitcoin.

Even though it is a decentralized system and perhaps the most secure and trusted crypto asset on the market, the U.S. and U.S. companies are among its largest holders, which means that using it may fail to achieve a radical competitive advantage.

At the same time, China’s massive purchase of Bitcoin may suggest that this option is possible, or at least Bitcoin will play a key role in this system even if they create their own blockchain with their own native cryptocurrency for every type of transnational trade.

Conclusion

We may be watching right now as the world accelerates into a new order of distributed trading systems, political blocs, and blockchain-based cross-border digital currencies where blockchain was the very last piece of the puzzle needed to make it all possible.

If this is the case, blockchain will change far more than perhaps even the most optimistic crypto enthusiasts, going far beyond decentralized finance to a decentralized distributed global economy and politics.

However, at moments of such fundamental change, we need to be especially careful and alert, and critically evaluate every aspect of every event, going deeper than what is being said about it, and thinking about everything that might be behind it.

Stay tuned for a comprehensive and detailed analysis of fundamental processes.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.