Latest news about Bitcoin and all cryptocurrencies. Your daily crypto news habit.

On October 10, 2022, the European Parliament Committee approved The Markets in Crypto Assets regulation bill (MiCA) and the European Parliament also voted on the Transfer of Funds Regulation (TFR).

It will be a milestone for crypto regulation in the EU once MiCA is in place. The FTX incident would not have happened if regulations of various countries on crypto assets have been properly implemented. In MiCA, terms of regulations on brokerage service providers, i.e., crypto exchanges, and issuing entities of stablecoin are clearly defined and strictly enforced. Not only can MiCA cement the fragmented regulatory landscape of countries in the EU to an integrated whole, but also have great influence on legislations on crypto assets all over the worlding, promoting the crypto market from wild growth to a lawful era.

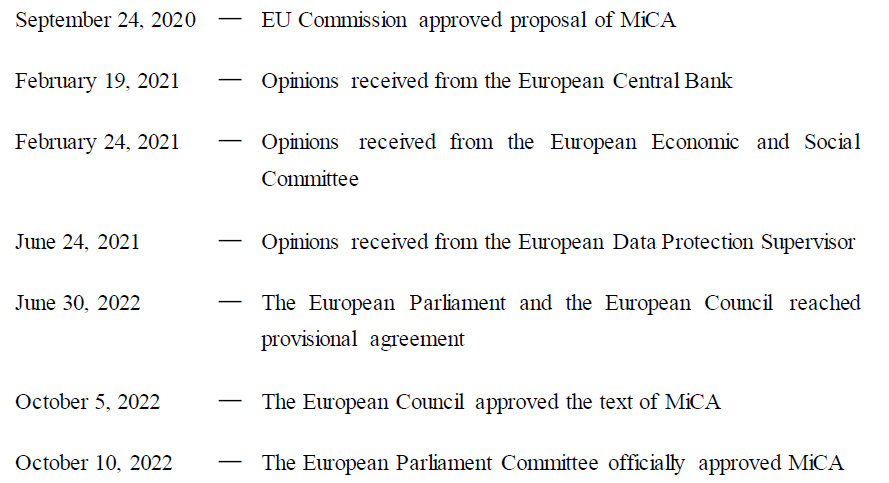

Recall the timeline of MiCA:

MiCA was originally scheduled for a final vote in plenary this November, but an EU spokesperson recently announced a delay to Feb 2023 as the draft needs to be translated into 24 languages; another 12–18 months will also be needed after MiCA is legislated in order that regulators in the EU have sufficient time to draft and apply new rules based on the legislation, and it is expected to be effective as early as February 2024. The initial approval of MiCA was expected to be in June, but it was not until October; the actual implementation is also expected to delay. Although plans on MiCA were repeatedly postponed, the significance remains to the crypto industry.

This article will analyze and interpret MiCA from perspectives of targeted types of crypto assets, approaches, and influences on the crypto market.

Why MiCA Deserves Attention?

First, MiCA is legislated on an upper-level that can be universally applied. The EU has no other unified regulatory framework on crypto assets but AML before; after MiCA is in effect, it is applied to the whole EU and superior to legislations of member countries; MiCA also authorizes extra power of enforcement to regulatory parties of member countries. Service providers of crypto assets will only need to comply with the requirements of one regulatory framework to operate within the 27 EU member countries with 500 million consumers; the costs for compliance of relevant entities will be greatly reduced.

Second, MiCA clarifies the regulatory rules for crypto assets such as stablecoin and crypto asset service providers (CASPs), providing clear guidelines for market participants and ensuring the healthy development path of the industry, which is conducive to enhance consumer protection and market confidence.

Finally, MiCA may serve as an exemplary existence that affects countries all over the world on legislations of crypto assets. Although the rapid development of the crypto market has produced financial innovations such as DeFi and NFT, problems are accompanied, such as money laundering, tax evasion, fraud, flee of assets, and encouragement of terrorism. Many countries in the world are actively exploring in regulatory framework of crypto assets, and MiCA, as an advanced regulatory framework in major judicial areas in the world, it may not only provide a reference for the legislation of some countries, but also promote some conservative countries to reverse negative attitude towards crypto assets.

Targeted Types of Crypto Assets in MiCA

The main regulatory elements of MiCA include: firstly, regulatory requirements for payment-based tokens such as stablecoin and other crypto assets; secondly, regulatory requirements for various crypto asset service providers such as issuers, providers, trading platforms, etc.

MiCA specifies the scope of application, the classification of crypto assets, the respective regulatory body and the corresponding information reporting system, restrictions of business conduct and behavioral regulation system, etc. MiCA establishes a regulatory framework for crypto assets that are not regulated by the existing EU financial laws, and crypto assets that qualify as financial instruments will not be regulated by MiCA, for example, security tokens and central bank digital currencies are excluded from MiCA.

MiCA enforcement will be administered by regulatory bodies designated by each member country in publication. The regulatory bodies may be new or existing institutions, and the European Banking Authority (EBA) and the European Securities and Markets Authority (ESMA) serve as regulatory bodies at the EU level.

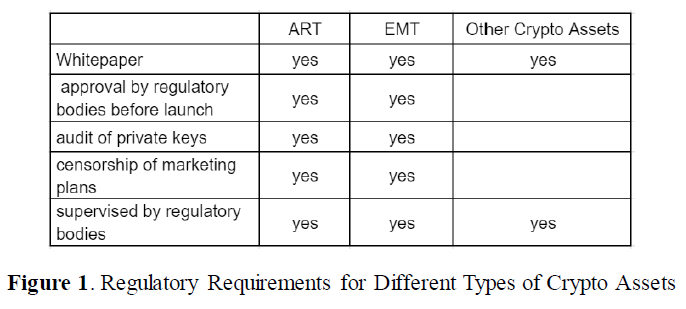

MiCA classifies crypto assets into electronic money tokens (EMT) and asset-referenced tokens (ART), and other crypto assets depending on whether there is an underlying asset.

● EMT is an electronic alternative to coins or banknotes that pegs the value by referencing to one type of fiat currency, in other words, it can be deemed as “electronic money”, it is commonly seen in various payment processing tools on Internet, such as Alipay, WeChat Pay, etc.

●ART pegs the value by referencing to other values or rights, which may include one or more fiat currencies; ART covers all other crypto assets backed by assets other than EMT. For example, USDT and USDC, which are stablecoin backed by US dollars and US treasury bonds, and Pax Gold, which backed by physical gold assets.

● Other Crypto Assets are all other crypto assets other than EMT and ART. Compared to EMT and ART, regulations on other crypto assets are relatively loose, requiring only the submission of whitepaper, approval, and compliance with general regulatory rules in marketing, organization, and technology.

Exemptions of MiCA:

● Other crypto assets acquired for free. The definition of “free” in MiCA is clarified strictly enforced: crypto assets that acquired by exchanging personal information, paying membership fees, commissions, monetary or non-monetary benefits, are not crypto assets acquired for free by definition.

● Crypto assets that are rewarded for maintaining distributed ledger technology (DLT, distributed ledger technology) or validations of transactions, such as Bitcoin.

● Utility tokens used in exchange for goods or services. In the case of utility tokens for goods and services that are still yet to be ready, MiCA applies for those with planning period over 12 months.

● Crypto assets that are unique and not fungible with other crypto assets, i.e., an NFT (MiCA does not use the term “NFT” directly in the text).

Regulatory Approaches of MiCA on Stablecoin, DeFi and NFT

MiCA will protect consumers by requiring stablecoin issuers to establish sufficient liquidity reserves at a ratio of 1:1 and partially in the form of deposits. Each holder of respective stablecoin has the right to claim holdings as issuer’s liability at any time, and the rules governing the operation of the reserve will provide sufficient minimum liquidity. All types of stablecoin will be regulated by the European Banking Authority (EBA).

Defined in MiCA, daily number of transactions must not exceed 1 million and trading volume for non-euro-backed stablecoin must not exceed 200 million euros. Currently, the three major stablecoin, USDT, USDC and BUSD, which account for more than 75% of cryptocurrency trading volume, have significantly exceeded MiCA’s terms on daily number of transactions and trading volume. If the EU is persistent on pursuing regulatory policies regarding non-euro stablecoin in the future, it may hinder the competitiveness and potential in innovations of the EU crypto market.

MiCA has not included DeFi in the scope of regulation for the time being because the DeFi information structure is different from traditional finance so that standardized policies cannot effectively regulate DeFi. The EU is piloting an “embedded regulation” solution for DeFi. On September 28, a public auction for a study of “ embedded regulation of DeFi on Ethereum” was initiated on the EU website; the budget is around 250,000 euros, and the duration of study is expected to be 15 months. The “embedded regulation” solution will endow regulatory parties with ability of autonomous surveillance on compliance by reading on-chain data, alleviating the demand for market participants on active collection of data, validations and submissions to respective regulatory bodies.

NFTs are also temporarily excluded from MiCA. According to MiCA, crypto-assets that are unique and not fungible with other crypto-assets are outside the scope of this regulation, and the European Commission will need to assess and establish a regulatory regime for non-fungible tokens (NFTs) within 18 months. MiCA does not insert the commonly used terminology “NFT” but describe such crypto-assets with the principle of nature over appearance: the value of an NFT is constituted by the uniqueness and functionality; it cannot be priced by any single pricing mechanism or measured by any single asset class. Therefore, an F-NFT (Fractionalized NFT) will not be considered a unique or non-fungible crypto asset; at the same time, an excessive amount of NFT issuance would be considered fungible in nature and subject to regulations of MiCA.

Will the Exceptionally Stringent Transfer of Funds Regulations (TFR) Stand?

TFR was first submitted to the European Commission in July 2021 as part of the EU’s ongoing legislative measures to improve anti-money laundering (AML) and counter-terrorist financing (CTF).

Under TFR, no cryptocurrency can be transferred between accounts of crypto asset service providers (CASPs) without complete KYC, which is stricter than the €1,000 threshold set as travelling rules by regulations in traditional financial sector. A transfer from a client of crypto exchange to a non-custodial wallet address cannot proceed by CASP without initial KYC indicating that the wallet address belongs to the sender. Transfers between two non-custodial wallets are not regulated by TFR.

Feedbacks vary from the EU public, which supporters arguing that it will help clarify regulatory boundaries for CASPs, but more are opponents with concerns on inability of market participants to comply with the technical requirements of the rules, and the collection of personal data may not necessarily impede money laundering, not to mention TRF violates the privacy terms in the Charter of Fundamental Rights of the European Union. With the postpone of vote on MiCA to February 2023, the legislative work on TFR may also be delayed, and many are expecting some adjustments in the final text that fully taking the specialty of crypto assets into consideration yet not deviating from the ultimate regulatory goal of improving the transparency.

The Significance of MiCA for the Industry

The four fundamental objectives of MiCA are: establishing a regulatory framework for crypto assets, providing supports to innovative activities and fair competition in crypto markets, enforcing consumers/investors protection and market integrity, and ensuring the stability of the financial system. A number of critical changes are expected to be seen after MiCA and TFR are implemented:

(1) A unified system of regulation and enforcement will be formed within the EU. MiCA enforcement will be managed by a designated authority in each member state, and the European Banking Authority (EBA) and the European Securities and Markets Authority (ESMA) are in charge on the EU level, to be more specific, a Crypto Asset Service Provider (CASP) is legitimate within the EU as long as it is registered and approved in any member state of the EU.

(2) Information reporting system and restrictions on business conduct are specified on object under regulations, i.e., crypto projects and crypto asset service providers (CASPs), to be more specific, contents of marketing communications, release and revision of information of crypto projects are regulated.

(3) Consumers will be under proper protection, and behaviors such as crypto market manipulation and insider trading are prohibited. For instance, stablecoin projects and crypto asset service providers (CASP) have clear requirements on reserve; a project with more funds and possibly more influence on the market will have more exposure to be regulated, which can effectively prevent incidents in the future similar to FTX.

(4) Regulations are stricter on critical assets, and more room are available for innovations. Boundaries of regulations are clearly defined on critical and mature crypto assets, while underdeveloped crypto assets, such as NFT and DeFi, are excluded from current regulatory framework with the intention not to hinder innovations.

(5) Crypto asset tracking, anti-money laundering and anti-terrorism are further strengthened. TFR extends the “travel rule” to all crypto asset transactions by removing the minimum threshold and exemptions low-value transfer; it is mandatory for both parties to fully disclose personal information containing source of funds and affiliated beneficiaries when trading on a crypto asset service provider (CASP) platform.

The implementation of MiCA ensures a unified regulatory framework that is effective in 27 member states throughout the EU, so that the burden of crypto projects and exchanges on costs of compliance and expansion in various jurisdictions within the EU will be relieved, and users of crypto assets will enter a market with more liquidity and opportunities as the market is now bigger. Except for specifications on information disclosure, reserve, marketing communications and operations, crypto companies are prohibited to receive interest on deposit of stablecoin; more regulations are coming out for intermediaries such as centralized exchanges, which may be uncomfortable to some crypto exchanges that are used to “wild” growth as they will be facing more restrictions, and more funds and institutions in traditional finance may find it an appropriate timing to enter as the portal is somewhat clean in the eyes of authorities. The positive implications of MiCA for the crypto industry outweigh the negative ones, as a regulated market is more conducive to the overall development of crypto assets, and smaller cryptocurrency exchanges and startups may benefit more from MiCA than large exchanges and crypto projects such as Binance.

Finally, MiCA and TFR are merely the beginning of the crypto market to be regulated in the EU; more changes and uncertainties may still be on the table in the future. A number of terms of censorship are found in MiCA and TFR, and a large number of subjects will be reviewed and reevaluated 1–3 years after the effectuation, such as non-custodial wallets, NFTs, and the sustainability of the acts. In addition to MiCA and TFR, the EU is also in the middle of several initiatives that will have significant impact on the crypto market, such as the DLT sandbox, the Digital Operational Resilience Act (DORA), the “embedded regulation” in DeFi, the NFT report, and legislations on digital Euro.

References

1. https://data.consilium.europa.eu/doc/document/ST-13198-2022-INIT/en/pdf

2. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2018.156.01.0043.01.ENG

4. https://ec.europa.eu/commission/presscorner/detail/en/ip_21_3690

5. https://twitter.com/paddi_hansen/status/1555869056594432005

6. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020PC0593

7. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52021AB0004

8. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52020AE4982&rid=1

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as “Huobi Research Institute”) was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of the blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Contact us:

Website:http://research.huobi.com

Email:research@huobi.com

Twitter:https://twitter.com/Huobi_Research

Telegram:https://t.me/HuobiResearchOfficial

Medium:https://medium.com/huobi-research

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The information and data cited in this report are from compliance channels. The Sources of the information and data are considered reliable by the author, and necessary verifications have been made for their authenticity, accuracy and completeness, but the author makes no guarantee for their authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

4. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the Source. If you need a large amount of references, please inform in advance (see “About Huobi Blockchain Research Institute” for contact information) and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent.

Tightening Global Regulations:Capability of MiCA Led by the EU was originally published in Huobi Research on Medium, where people are continuing the conversation by highlighting and responding to this story.

Publication date

Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not reflect the views of Bitcoin Insider. Every investment and trading move involves risk - this is especially true for cryptocurrencies given their volatility. We strongly advise our readers to conduct their own research when making a decision.